US employers are gradually dialing back the pace of hiring and hourly earnings are moderating, offering some solace to Federal Reserve policymakers in their bid to wrangle still-elevated inflation.

For investors, though, economic data and monetary policy have taken a back seat to negotiations on the federal debt ceiling that are stretching into the final days before the US government risks defaulting. While lawmakers have narrowed differences, a final deal has yet to be struck.

Government data on Friday are projected to show payrolls in the world’s largest economy increased by less than 200,000 in May, down from average monthly job growth of about 370,000 over the past year. Earnings are seen rising 0.3% from the prior month, when they posted the biggest advance in a year.

Another report in the coming week is forecast to show the fewest open positions in two years. Although vacancies are still about 2 million above pre-pandemic levels, a fourth-straight monthly drop in April job openings would underscore a gradual loosening of the tight labor conditions that helped fuel inflation over the past year.

The latest snapshots of the labor landscape will provide Fed officials with clues about the impact from tighter credit conditions, higher interest rates and brewing economic concerns.

Policymakers next meet on June 13-14 to decide whether another quarter-point hike in the benchmark rate is warranted after data this week showed faster inflation and resilient demand at the start of the second quarter.

Fed officials scheduled to speak in the coming week include regional bank presidents Thomas Barkin of Richmond and Patrick Harker of Philadelphia, along with board member Philip Jefferson.

What Bloomberg Economics Says:

“May jobs data are expected to show a slowdown in the pace of hiring — but not enough to put the Fed at ease. The choppiness of the monthly payroll data masks a gradual slowdown in the hiring pace since late-2021 — though the labor-market cooling has been slower than most analysis expected.”

—Anna Wong, Stuart Paul, Eliza Winger and Jonathan Church, economists. For full analysis, click here

Further north, Statistics Canada will reveal gross domestic product for the first quarter, providing crucial insights into whether the economy is cooling enough for the Bank of Canada to hold rates steady next month.

Elsewhere, data showing slower euro-zone inflation, surveys of Chinese purchasing managers, and multiple GDP reports may grab investors’ attention.

Click here for what happened last week and below is our wrap of what else is coming up in the global economy.

Asia

Chinese purchasing-manager indexes will be a highlight in the region. On Wednesday, the official PMI is predicted by economists to show the deterioration in manufacturing easing slightly, while robust growth in the non-factory gauge is expected to slow.

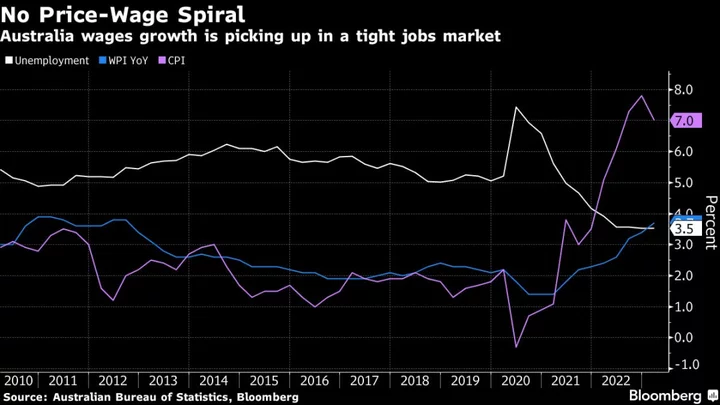

Australia’s inflation number for April, due the same day, may prove pivotal for observers of the Reserve Bank. The median forecast is for a slight acceleration, to 6.4%, though some economists reckon it will stay at the same pace or even slow.

In India, GDP data for the first quarter out on Wednesday may show a pickup, with both domestic and overseas demand helping to boost growth.

Thailand’s central bank is likely to raise its rate by a quarter point the same day, with Sri Lankan officials also due to deliver a verdict on monetary policy.

And in Japan, industrial production on Wednesday is expected by economists to have increased for a third month in April.

- For more, read Bloomberg Economics’ full Week Ahead for Asia

Europe, Middle East, Africa

The latest reading of euro-zone inflation on Thursday may draw significant attention, with the data expected to show frustratingly slow progress for the European Central Bank in tamping down price pressures.

Headline consumer-price growth is seen weakening to 6.3% in the 20-nation currency area, while the underlying measure that strips out volatile elements such as energy may be little changed at 5.5%. Both readings would remain well above the ECB’s 2% target.

National reports before then will probably underscore divergence across the region. Spanish inflation on Tuesday is expected to slow to 3.3%, while readings in France, Italy and Germany the next day may all remain above 6%.

Central-bank governors from Croatia, Austria and Italy are among the ECB policymakers scheduled to speak, and minutes from the May 4 meeting will be released on Thursday.

The institution’s latest financial-stability report, due the previous day, will also draw attention, not least after banking-sector turmoil in the US and Switzerland.

It’ll be quiet in the UK, which starts the week with a public holiday, as does much of Europe. A speech by Bank of England official Catherine Mann on Wednesday and consumer-lending data the next day are among the main events there.

Swiss GDP on Tuesday may show the economy barely growing in the first quarter after flat-lining the prior three months. That’s still respectable considering the economy’s integration with that of Germany, which suffered a recession.

Swedish first-quarter GDP data will be released the same day, with no growth anticipated by economists after a drop in the prior period. The European Commission predicts the country will face the European Union’s worst economic slump in 2023.

Several Russian reports will be published on Wednesday, including industrial production, weekly inflation, retail sales, wages and unemployment.

Looking south, Turkey releases growth data on Wednesday. The election there will be closely watched as President Recep Tayyip Erdogan faces Kemal Kilicdaroglu in a runoff on Sunday.

Erdogan did better than polls predicted in the first round on May 14, falling just short of the 50% threshold needed to avoid another round of voting. The markets favor him to secure another term.

In Africa on Monday, Kenya’s rate-setting committee is poised to leave borrowing costs unchanged as it monitors the impact of a jumbo hike in March after inflation softened last month.

The following day, Lesotho, whose currency is pegged to South Africa’s rand, will probably follow its neighbor and hike rates. And on Wednesday, nearby Mozambique’s officials may keep the benchmark rate steady for a fourth straight meeting.

- For more, read Bloomberg Economics’ full Week Ahead for EMEA

Latin America

The minutes of Banco Central de Chile’s May 12 meeting, to be released on Monday, will likely echo the post-decision communique’s central takeaway: the slow pace of disinflation gives policymakers little choice but to hold at 11.25% for the foreseeable future.

The minutes of Banxico’s May 18 meeting should underscore the board’s concern that the inflationary outlook is “complicated and uncertain,” so the Mexican central bank will need to keep rates high — they’re now at a record 11.25% — and stable for an extended period of time.

Banxico’s quarterly inflation report posted mid-week may see economic output forecasts raised while those for inflation are revised down on the back of a strong peso and a jump in foreign investment fueled by near-shoring.

Four of the region’s big five economies will release unemployment data. Joblessness is heading back up in Brazil and Chile after recovering from pre-pandemic levels, hovering near post-pandemic low in Colombia, while sitting at a record low 2.39% in Mexico.

Latin America’s biggest economy likely rebounded in the first three months of 2023 on one-time factors such as government social stipends and a strong harvest. Most analysts see Brazil heading into at least four years of below-average growth, posing a significant challenge to President Luiz Inacio Lula da Silva’s agenda.

- For more, read Bloomberg Economics’ full Week Ahead for Latin America

--With assistance from Robert Jameson, Laura Dhillon Kane, Monique Vanek and Paul Richardson.