Sweden’s largest bank says the nation’s lenders are strong enough to support the turbulent property markets, even as funding costs and their exposures are rising.

“There is blood running in the streets in Sweden but not in the bank sector,” SEB AB Chief Financial Officer Masih Yazdi said in an interview in Visby last week about the state of the commercial property market.

Sweden’s real estate market has become one of the main arenas where the impact of central banks’ rate hikes are playing out, blowing holes into landlords’ business models that for years were based on debt-fueled expansion. The rising cost of refinancing has pushed many to slash payouts and sell assets to repay maturities. Property companies are also turning to banks for funds.

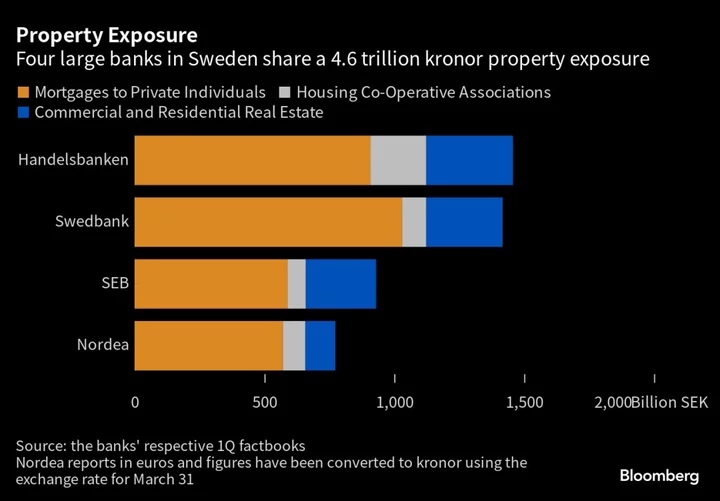

SEB, as well as its peers Swedbank AB, Svenska Handelsbanken AB and Nordea Bank Abp, have pledged to help core clients that are seeking to replace maturing bonds with bank loans as funding costs in the credit market have skyrocketed. They already share an exposure totaling nearly 4.6 trillion kronor ($419 billion) between them, but that number could grow by around 60 billion kronor this year, as a very rough estimate, Yazdi said.

“Everyone can see that all the banks’ funding costs have risen, that share prices have declined and that the Swedish krona has weakened,” Yazdi said. “So there is a heightened risk premium on Sweden today because of the real estate sector, and it also weighs on banks since they play such an important role.”

In the absence of “huge credit migration,” the CFO said he’s not worried that the bank will need to retain more capital than planned as credit quality deteriorates. Sweden’s FSA holds the nation’s banks to a higher standard than Basel models would suggest, justifying its stance by the sizes of the Nordic nation’s commercial real estate and mortgage markets and the importance to both individual credit institutions and financial stability in Sweden.

SEB, in line with the rest of the industry, has benefited from central banks’ rate increases, which allowed them to charge more for loans while rates on checking accounts have been kept at zero until very recently, letting the banks pocket the difference. Lenders are, however, getting closer to a turning point as interest rates approach their peak.

Sweden’s central bank last week raised its benchmark rate by a quarter point to 3.75% and said it expects to lift it at least one more time this year.

Yazdi said the contribution from rate hikes to the bank’s net interest income is getting close to zero. Higher rates are also beginning to weigh on borrowers’ credit quality, but the deterioration is “very small and rather undramatic so far,” he said.

SEB is scheduled to present its second-quarter report on July 18.

--With assistance from Thomas Hall.