Global debt markets are bursting with new deals as September kicks off, with investment-grade companies rushing to lock in borrowing costs before central bankers can raise them further.

At least 40 businesses tapped high-grade debt markets around the world on Tuesday, ahead of crucial releases of economic data and central bank policy decisions later in the month. About half of those deals — or over $36 billion of new bonds — were sold in the US, making it the busiest session in terms of deal count and daily supply so far this year, according to data compiled by Bloomberg.

BHP Billiton and Philip Morris International Inc. are among those that brought deals in the US after the Labor Day holiday, while banks featured prominently in a flurry of Asian primary market activity. Businesses across the euro zone, meanwhile, sold at least €18.7 billion ($20.1 billion) Tuesday, with the week’s volume forecast at more than €25 billion.

“I would expect companies to be trying to get ahead of any economic data that sends US Treasury yields higher,” said Winnie Cisar, global head of credit strategy at CreditSights. “I think we will see a front-loaded issuance month.”

The month’s early wave of issuance comes after a recent slowdown, tied to both regular summer trends across the northern hemisphere and a recent rise in US Treasury yields. But with September comes a strong seasonal precedent for issuance, according to Cisar, especially for investors who believe that policymakers are close to claiming victory against sticky consumer price gains.

Money managers from BlackRock Inc. to Pacific Investment Management Co. are starting to bet that the Federal Reserve’s tightening cycle is finally ending, echoing a similar sentiment across global financial markets. Companies are seeking to make the most of the positive mood while they can, especially ahead of crucial events such as an upcoming reading of US inflation data and the Fed’s Sept. 20 meeting.

In the US, BHP priced $4.75 billion of fresh debt in a five-part deal of senior unsecured notes, with the longest dated portion of the offering — a 30-year note — yielding 1.25 percentage points over Treasuries. Philip Morris also tapped markets for a $2.35 billion, three-part deal on Tuesday.

The gush of fresh investment-grade supply, alongside a surge in oil prices, helped push Treasury yields higher.

That activity comes in contrast to a more muted start on Tuesday for US leveraged finance markets. Heartland Dental is planning to sell an additional $100 million of its 10.5% bonds due 2028, while Sally Beauty Holdings Inc. is launching a deal to reprice a term loan. Still, investors are bracing for a wave of new issuance in the coming weeks, more than $15 billion of which is tied to leveraged buyouts.

Representatives for BHP, Philip Morris, Heartland Dental and Sally Beauty didn’t respond to requests for comment.

Read: Recession Risk Looms Over Pricing in September Bond Sales Rush

To David Knutson, senior investment director at Schroder Investment Management, the firehose of fresh US debt supply “will continue to spray until the market is flooded” as investors grow increasingly comfortable with the idea of a soft landing for the world’s top economy. That “belief can and is influencing the thoughts and behavior of the market,” he said.

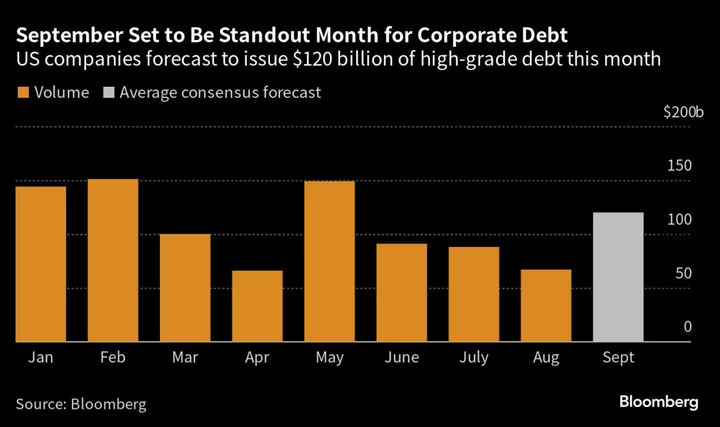

A survey of bankers who underwrite the deals forecast $120 billion of US debt to be issued in September, much of which is expected to be sold in the next few days.

Issuance has already picked up across Europe, with nearly €48 billion of debt sold by the region’s companies and financial firms over the past two weeks, according to data compiled by Bloomberg. Even so, European borrowers will likely need to offer investors better terms on bonds against the backdrop of a potential recession in that region.

“The US is defying the economic gravity that is pulling down China and Europe,” said Knutson. “The primary market tends to produce supply until investor demand is satiated. Given how low volatility is and tight credit spreads are, I would expect supply to continue until the market gets swampy.”

--With assistance from Ronan Martin, Michael Gambale and Allison Nicole Smith.

(Updates with US debt sold Tuesday in second prargraph. Updates deals throughout.)