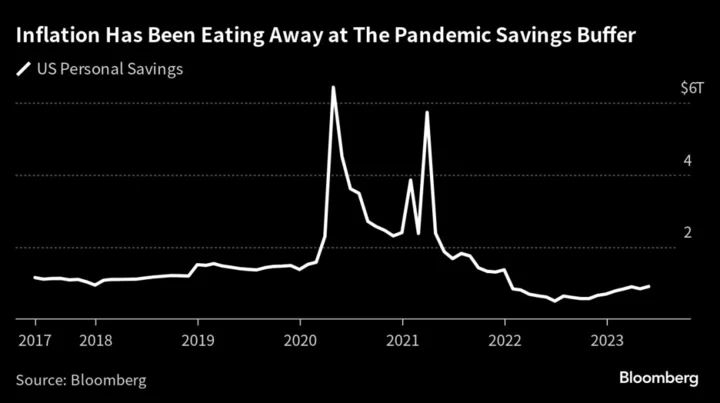

US consumers, particularly those with lower incomes, are running into financial trouble as pandemic savings disappear, a headwind for lenders ranging from banks to asset-backed securities investors.

The credit outlook is expected to deteriorate later this year when almost 27 million borrowers have to resume making payments on student loans. Delinquencies for other forms of debt will likely rise, as people divert money away from servicing car loans and credit cards, according to Morgan Stanley economist Sarah Wolfe.

Consumer spending growth will likely also face pressure as debt servicing burdens rise. Bank of America Corp. Chief Executive Officer Brian Moynihan pointed out in the latest week that consumer spending patterns now are consistent with slowing growth in the economy.

Some are already suffering. Bloomberg Economics estimates that the average household in the bottom 40% of income distribution now has $1,200 less liquid assets than they did before the pandemic when adjusted for inflation.

“Savings, at least in the lower income cohort, have disappeared,” Tracy Chen, a portfolio manager at Brandywine Global Investment Management, said in an interview. “With banks tightening their lending standards, consumers are going to have a hard time getting credit.”

The rejection rate for credit cards, mortgages, and mortgage refinances all rose in June from February, according to a Federal Reserve Bank of New York survey, limiting the options for borrowers with a shaky credit history. The collapse of Silicon Valley Bank is also crimping consumers’ ability to borrow as some regional banks focus on tightening standards in the wake of the turmoil.

The trend of the riskiest borrowers struggling can already be seen in the auto market. The delinquency rate for prime auto loans ticked up to the highest level for the month of May in 12 years, according to data from S&P Global Ratings. It was the highest on record for May for subprime borrowers.

“It’s just going to get worse,” John Toohig, head of whole loan trading at Raymond James & Associates, said in an interview. “I am very bearish when it comes to subprime auto. Those delinquencies will end up creeping into prime.”

That signals potential pain ahead for lenders of all kinds. Citigroup Inc., the world’s second biggest credit card issuer, posted a 78% surge in write-offs tied to consumer loans for the latest quarter. The company said its net credit losses are normalizing and are still below pre-pandemic levels.

Some bonds tied to car loans made by U.S. Auto Sales and American Car Center veered into distress in recent weeks after borrowers fell behind on payments. Citigroup believes that some of the riskiest parts of those asset-backed securities could fail to return principal to investors.

Retail Pain

Consumer cutbacks mean some private equity-backed retailers are also hurting. Fishing gear business Pure Fishing Inc. has tapped advisors as it faces liquidity pressures due to weak demand and department store chain Belk Inc. told creditors it expects weaker revenue in 2023.

To be sure, US consumer sentiment is still high, soaring as inflation eases and the labor market remains strong. But that could quickly change if the economy slows further.

“The job market is key and unemployment is still low, but when it starts going up, it’ll be quick,” said Chen at Brandywine. “We’ll soon see consumer pain spilling onto Wall Street.”

Week in Review

- Wall Street banks flooded the US investment-grade bond market: Morgan Stanley sold $6.75 billion of debt, JPMorgan Chase & Co. sold $4.5 billion and Wells Fargo & Co. sold securities including $8.5 billion of fixed-to-floating-rate notes.

- Chinese property companies experienced a new bout of debt setbacks, raising questions even about developers seen as among the strong firms. Shui On Land Ltd. said it was seeking to identify bondholders, a step often foretelling payment delays. State-backed peer Sino-Ocean Group Holding Ltd. halted trading in a local note that matures in two weeks, flagging “significant” uncertainty in repaying that security.

- China Evergrande Group is looking to meet offshore creditors to win their approval for its overhaul plan, seeking to complete one of the country’s biggest debt restructurings.

- Global corporate bond indexes hit their highest level this year on bets that the inflation crisis is coming to an end.

- Private credit firms are extending their reach into the more than $260 billion global asset-based lending business.

- In the tussle between public and private debt markets, Goldman Sachs Group Inc.’s underwrite for Kahoot! ASA means a win for the private side.

- A pact among Carvana Co. creditors to work together as they negotiated how to restructure the used-car dealer’s massive debt load reached a pivotal moment last month, during a meeting with Chief Executive Ernie Garcia.

On the Move

- Nomura Private Capital has hired Steve Kavulich as head of opportunistic private credit, according to a memo seen by Bloomberg. He joins from BlackRock Inc., where he was an opportunistic credit portfolio manager.

- Barclays Plc is tapping Scott Schulte to run its US high-grade syndicate desk. He had been with Citigroup Inc., where he was a managing director on its US investment-grade syndicate desk.

- Deutsche Bank AG has recruited high-yield bond trader Lisa Chow from Bank of Nova Scotia. Chow, who had been based in Toronto, will join the German lender’s trading desk in New York.

- TD Securities added Hans Mikkelsen from Wells Fargo & Co. as managing director of credit strategy, the latest move in the Canadian bank’s bid to expand its reach in fixed income.

- UBS is looking to bring on professionals including credit analysts for the collateralized loan obligation team in Credit Suisse’s asset management unit, and has also worked to keep key staff in the business.

--With assistance from Paige Smith, Reshmi Basu, Felice Maranz and Taryana Odayar.