With 46 straight days of 100-degree heat and coastal waters approaching hot-tub temperatures, Miami can seem like a clear example of the costs of a warming world. But analysts at S&P Global Inc. aren't sweating it.

They recently upgraded Miami’s credit rating, citing a robust tax base and labor market. The city’s “elevated” environmental risks, S&P says, are offset by mitigation projects such as those designed to counter rising sea levels.

As the world reels from the mounting impact of heat waves, droughts and fiercer storms, there is growing concern that credit rating analysts are misreading climate risks in the $133 trillion global bond market, to the detriment of creditors and borrowers alike.

Research by the European Central Bank shows that even when climate variables are statistically significant, they play only a marginal role in influencing sovereign ratings. And a study conducted by a Federal Reserve economist indicates that extreme weather events may end up restricting some governments’ ability to issue debt.

Climate change has “yet to be hardwired into the methodology” currently used by the biggest ratings companies, said Moritz Kraemer, who oversaw S&P Global’s sovereign debt ratings until 2018 and is now head of research at Germany’s LBBW Bank.

It’s only 15 years since S&P, Moody’s Investors Service and Fitch Ratings famously misjudged the subprime mortgage market that triggered the 2008 financial meltdown. Now, they’re under fire for potentially underestimating potential climate losses in a rating system more tuned to the near term.

S&P, Moody’s and Fitch say they do account for climate risks, though it isn’t an easy calculation. Since the start of 2022, S&P has published five climate-related ratings actions on non-financial companies. It says climate regulations have yet to bite and most companies’ net zero spending isn’t big enough to affect financials or ratings.

S&P Global said it evaluates the impact of ESG credit factors for its debt ratings. These factors include climate transition and physical risks, health and safety, and risk management. They can impact a rating if they're deemed to be material to creditworthiness and if S&P can measure their impact with enough certainty, according to a company spokesperson.

At Fitch, climate change and other environmental risks have affected about 6% of its ratings, though it expects that to change within the decade. Some 20% global corporations may face ratings downgrades by 2035 due to climate vulnerabilities, according to Fitch estimates.

Moody’s estimates that sectors facing high or very high environmental credit risk now account for $4.3 trillion in rated debt, a figure that’s doubled since late 2015. But when the Institute for Energy Economics and Financial Analysis, a nonprofit in Lakewood, Ohio, looked at Moody’s ESG credit scores for 721 companies in high-emitting industries, it found that about 60% of issuers with high credit ratings were highly exposed to environmental risks, including climate change.

A Moody’s spokesman said the company “systematically, consistently and transparently” incorporates credit-relevant ESG factors, including climate risks, into its ratings.

Credit rating companies need to move more swiftly, said Matthew Agarwala, an economist at Cambridge University. “They’re inching forward, but the icecaps are melting faster,” he said.

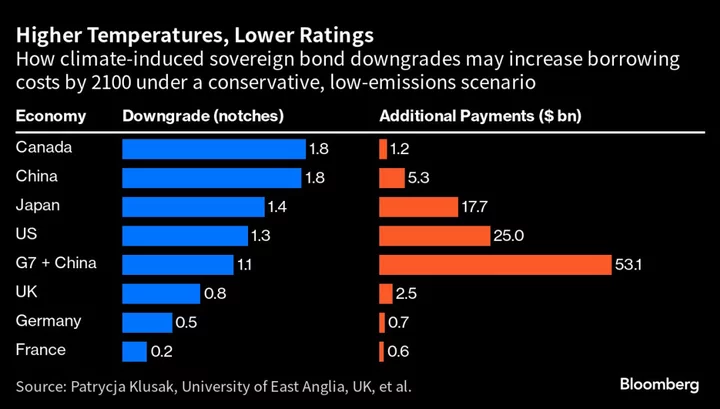

Agarwala, his Cambridge colleague Kamiar Mohaddes and Patrycja Klusak of the University of East Anglia have studied the impact of climate change on economic growth and sovereign debt markets. In a paper due to be published in the journal Management Science, they and other academics map out some of the loss scenarios.

For example, if climate risks were properly calculated under a conservative, low-emissions trajectory, 58 sovereigns would experience “downward pressure” on ratings by 2030. Chile and India would be among the worst hit. The affected countries’ annual interest payments would rise by as much as $67 billion under the moderate scenario, and up to $203 billion under a more extreme scenario.

Marc Painter, assistant professor of finance at Saint Louis University in Missouri, studied almost 20,000 long-term bond issuances. He found that a US county facing a 1% increase in climate risk pays an average $1.7 million more annually in underwriting fees and initial yields, compared with counties unlikely to be affected by climate change. That additional $1.7 million “implies a county with higher sea level rise risk will spend 5% more to issue their bonds," Painter said.

Central bank researchers, meanwhile, worry that a climate shock could tip a vulnerable sovereign issuer into default.

Enrico Mallucci, an economist at the Fed, examined the impact of hurricanes on seven Caribbean countries. Under a scenario forecast in climate-change literature—namely that the frequency of high-category hurricanes goes up 29% and their intensity increases 49%—debt spreads will increase more than 30%, he said.

“Extreme weather restricts governments’ ability to issue debt,” Mallucci said. And “extreme weather events and natural disasters are poised to become even more sizable in the coming years.”

As for the $3.8 trillion US municipal debt market, Tom Doe, president of the research firm Municipal Market Analytics Inc., said that as far as he knows, “no US municipal issuer’s credit rating has been changed because of climate change risk.”

In a report published last September, the ECB found that most ratings firms have made progress, but they still do a poor job of explaining their climate calculations, including transition and physical risk. “The magnitude of the impact of material climate change risk on credit ratings is rarely disclosed,” the ECB said.

Angela Maddaloni, a researcher at the ECB who wasn’t involved in the September report, said credit ratings currently don’t offer “good measures of certain climate risks.”

BlackRock Inc., Schroders Plc and other investment managers aren’t waiting for the ratings industry to catch up. They’re already designing products or selecting bonds based on climate risks that aren’t always captured in credit scores.

Saida Eggerstedt, head of sustainable credit at Schroders, recently declined to buy a green bond issued by Alliander NV, a Dutch electricity distributor. Moody’s rated the issue Aa3, but Eggerstedt was turned off in part because the firm lacks public climate targets and has a relatively high carbon intensity. “You can get frustrated when long-term, non-financial impacts aren’t reflected in credit ratings,” she said.

In 2020, BlackRock introduced a first-of-its-kind exchange-traded fund that weights debt issued by euro-zone sovereigns on the basis of exposure to climate risk. Belgium and the Netherlands are among countries with the lowest weightings due to their higher perceived climate exposure. It’s one of a number of similar ETFs that BlackRock is developing.

Such products “meet the growing interest from clients to mitigate risk and capture opportunities associated with climate and the transition to a low-carbon economy,” said Manuela Sperandeo, global head of sustainable indexing at BlackRock.

S&P, Moody’s and Fitch all acknowledge that climate change is likely to have a material impact on debt markets. The question is when —and whether the ratings will capture it before it’s too late.

Alex Griffiths, head of EMEA corporate ratings at Fitch, said that “if you go out even 15 years, we know very significant things are likely to be happening.”