The bond market is finally getting in sync with Jerome Powell’s outlook for the economy.

Traders have scrapped once-aggressive wagers that the Federal Reserve chief would pivot to easing policy before the end of this year, reflecting deeply diminished expectations that the central bank’s rate hikes are poised to set off a sharp recession. Bond yields have risen back toward levels seen before the panic sown by Silicon Valley Bank’s collapse.

And even with policymakers seeing a chance for two more rate increases in the months ahead, the US economy is expeted to hold up fairly well, unlike Europe’s, which is showing signs of stalling.

“A realization is setting in that the Fed isn’t going to be cutting interest rates this year,” said Greg Peters, co-chief investment officer PGIM Fixed Income. “It’s a kind of an ‘ah-ha’ moment being priced in by the market that central bankers mean what they say.”

US Economy Seen Skirting Recession But With Sticky Inflation

The divergent outlooks in the US and Europe were underscored Friday, when S&P Global purchasing managers indexes indicated that growth nearly stalled in the euro area this month but continued in the US, albeit at a slower pace. The reports fueled a large rally in the European government bond market as investors shifted into havens, with US Treasuries posting smaller gains.

Nevertheless, the figures highlighted the risk of a slowdown in global growth that would weigh on the US. And markets have been anticipating that the economy will slow, even if the US only narrowly avoids a recession this year.

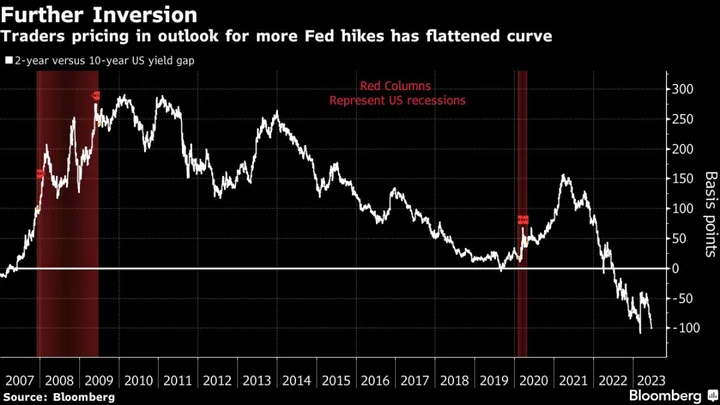

After Powell told US lawmakers this week that more rate hikes are likely, 10-year yields slipped to a full percentage point below 2-year rates, deepening a yield curve inversion that’s usually seen as a harbinger of a recession. But that was largely because of an upward jump in short-term rates as longer-term ones held little changed.

While swaps traders have pushed out the expected cuts until next year, they expect that the Fed’s key rate will still remain high enough to curb growth. That means policymakers are still expected to be focused on inflation, not trying to jump-start growth.

Powell told the Senate Banking Committee on Thursday that “we will do what it takes to get inflation down to 2% over time.” He said that two more rate hikes were possible this year and he didn’t see a reduction in rates “happening anytime soon.”

Powell will be speaking this coming week at several global events, potentially giving more insights on the policy outlook.

The release Friday of the Fed’s preferred inflation gauges are expected to show some improvement in May after surprisingly hot readings from April, a result that would lend additional momentum to bond traders seeing more calm ahead. Already, both short- and long-run consumer-price inflation expectations have held steady at just over 2% since early May on anticipation that the Fed will succeed in its mission.

The personal consumption expenditures price index is forecast to slow to an annual pace of 3.8% in May from 4.4% in April, according to economists surveyed by Bloomberg. The core measure, which excludes food and energy, is predicted to hold steady again at a 4.7% level.

“If you look at some of the indicators of inflation in the US, they are clearly coming down,” Thierry Wizman, global interest rates and currency strategist at Macquarie, said on Bloomberg television. “In the back half of the year you are going to finally see that so-called stickiness we are seeing in” several inflation indices “start to recede and come down. I think the market understands that.”

With the outlook growing less uncertain, the swings in the bond market have been less severe. That’s also a positive sign for traders, many of whom had come into 2023 predicting a better year for bonds, which have gained about 1.6%, rebounding slightly from the deep losses of 2022.

The ICE BofA MOVE Index, a closely watched proxy of expected Treasury swings, has tumbled by nearly half since March, when it reached the highest since 2008.

Traders see another quarter-point hike in July now as likely and give some chance to another. The Fed’s policy rate is seen peaking this year at around 5.35% before the US central bank pushes rates to around 3.8% by December 2024, a level that’s still what’s considered high enough to slow economic growth.

“Given how far we’ve come, it may make sense to move rates higher but do so at a more moderate pace,” said Jared Gross, head of institutional portfolio strategy at J.P. Morgan Asset Management

What to Watch

- Economic data calendar

- June 26: Dallas Fed manufacturing index

- June 27: Durable goods; FHFA house-price index; S&P CoreLogic Case-Shiller home prices; new-home sales; Conference Board consumer confidence; Richmond Fed manufacturing index and business conditions; Dallas Fed services activity

- June 28: MBA mortgage applications; wholesale inventories; advance goods trade balance; retail inventories

- June 29: Weekly jobless claims; gross domestic product report; pending home sales

- June 30: Personal income and spending report, including PCE; MNI Chicago PMI; University of Michigan sentiment and inflation expectations

- Federal Reserve calendar:

- June 26: Powell will speak on a panel in Sintra with several other global central bank heads

- June 27: Powell takes part in a discussion hosted by the Bank of Spain

- June 29: Atlanta Fed President Raphael Bostic

- Auction calendar:

- June 26: 13- and 26-week bills; two-year notes

- June 27: 42-day cash management bills; five-year notes

- June 28: 17-week bills; two-year floating rate note; seven-year notes

- June 29: Four- and eight-week bills

--With assistance from Ye Xie.