In his four and a half years in office, Mexican President Andres Manuel Lopez Obrador has placated Pemex investors by repeatedly giving the state oil company cash bailouts and tax cuts.

Each time, the aid — around $77 billion and counting — temporarily alleviates pressures on the company’s bonds. Then, as quickly as it appeared, the rally fades.

The pattern has led to a growing sense of fatigue among money managers who hold the debt. They argue the handouts made by AMLO, as the president is known, have done little to solve the company’s deep structural problems or address growing questions about its governance and sustainability practices.

“This administration really is not making a concerted effort to address investor concerns,” said Edwin Gutierrez, a money manager at Abrdn in London. The latest capital injection is “good news in the near term as it clarifies any uncertainty over short-term financing. But obviously these governance issues will continue to weigh on the company.”

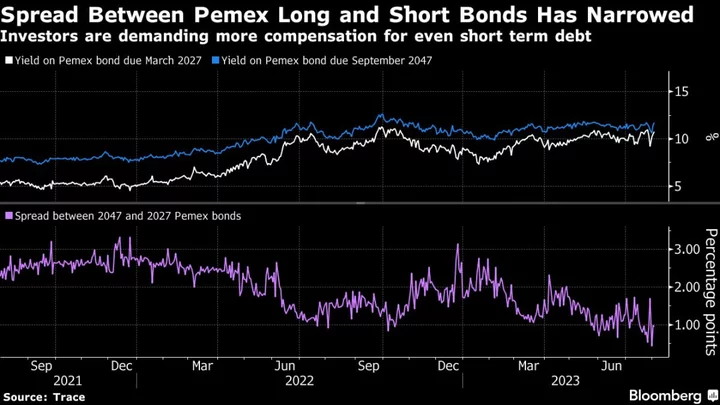

Investors are now demanding 600 basis points more to hold the oil giant’s notes due in 2027 than similar sovereign bonds, even though the company is entirely owned by the government. That’s about double the premium for bonds of South Africa’s troubled, state-owned energy company Eskom Holdings.

In a sign of how fed up markets have become with AMLO’s Band-Aid approach, it took just five days for the spreads on Pemex bonds to return to some of the highest levels in years after a brief reprieve when it announced it received a $4 billion handout last month.

The same pattern that has unfolded every time AMLO has stepped in. Whether it’s a capital injection or a reduction of Pemex’s massive tax burden, any rise in bond prices quickly fades as investors return their focus to the company’s mounting debt, dwindling oil production and lack of plans to tackle sustainability concerns.

On top of capital injections, AMLO has reduced the profit-sharing tax to 40% from 65% in the last four years, and taken every opportunity to voice his support for the driller. “Pemex isn’t a private company,” Lopez Obrador said during a morning press conference last month. “It’s connected to the nation.”

The capitalizations — 720 billion pesos ($42.2 billion) through the end of June — have been earmarked for debt repayment and investment, ranging from the construction of the Dos Bocas refinery to the purchase of Shell’s stake in the Deer Park plant and other refining and fertilizer projects.

Read More: Pemex Profits Fall Amid $4 Billion Government Injection

Even though the debt isn’t explicitly guaranteed by the government, AMLO’s repeated pledges to support the driller made the bonds a favorite for some emerging-market investors who are attracted by the yields.

As a result, Pemex debt has rallied since AMLO took office at the end of 2018, with a total return of 15.8%, compared to 4.5% for a broad emerging-market index.

But with his departure looming after next year’s election, the question has turned to how much support Pemex will receive going forward, said Claudia Calich, the head of emerging-market debt at M&G Investments.

“Some of the spread volatility is reflecting risks ahead for the election,” Calich said. “It’s difficult because it’s a bit of the ‘chicken or the egg’ — who do you blame? Do you blame the company for not being more efficient or do you blame the Mexican government?”

Some Wall Street giants including Pimco have limited themselves to short-dated bonds out of concerns the next administration won’t be so generous. Pemex bonds will face pressure as long as there is the lack of a plan for the medium term, said JPMorgan Asset Management’s Pierre-Yves Bareau, who oversees about $50 billion in emerging-market debt.

“There’s definitely a rhetoric in favor of Pemex,” he said. “Beyond that, there’s definitely a bigger issue for the Mexicans that they need to address.”

The questions over government support come on top of a litany of underlying concerns, including production that’s fallen roughly by half from two decades ago, inefficient refineries, and a ballooning debt burden. The $110.5 billion it owes ranks it as the most-indebted oil major in the world both as a total number and as a ratio of its earnings, according to data compiled by Bloomberg.

Read More: Pemex Says Size of Gulf of Mexico Spill Has Been Overstated

The operational woes have been brought into sharp contrast by a spate of recent incidents, including a deadly gas platform explosion in the Cantarell field complex last month, setting the ocean on fire, an oil leak nearby the site of the blast several days earlier, and a series of fires this year at half of its refineries.

That track record has alienated funds that are increasingly incorporating environment, sustainability and governance — known as ESG — standards into their portfolio. Pemex has yet to produce a long-awaited plan to address sustainability issues.

For Sergey Goncharov, an investor at Vontobel Asset Management who holds the debt, they’re all signs of a slow-motion downfall.

“It’s never a rapid demise,” he said, “but I’m turning more cautious lately.”

(Updates ninth paragraph with details on government support.)

Author: Maria Elena Vizcaino, Michael O'Boyle and Carolina Wilson