The powerful rally in small-cap stocks looks like yet another false start rather than a lasting recovery.

The Russell 2000 Index — the world’s most closely followed gauge of smaller companies — rose over 5% last week as softer US inflation data bolstered bets that interest rates have topped out. Still, it will be hard for the gauge to avoid notching its worst year since 1998 against a benchmark of larger peers, given how vulnerable it is to damagingly high debt costs and a potential economic downturn.

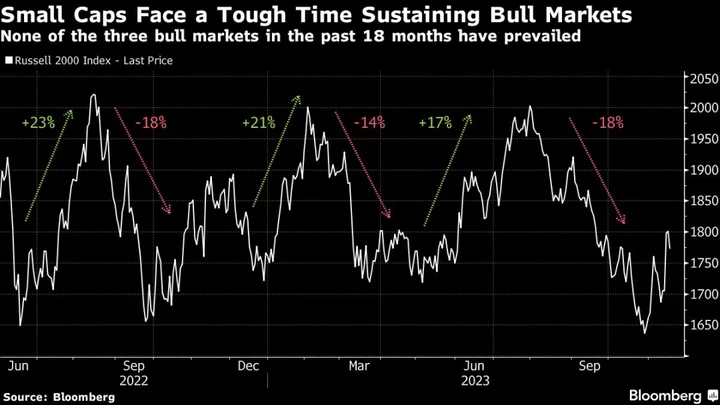

What’s more, unlike its bigger counterpart, the Russell small-cap index has tried and failed three times in the past 18 months to sustain a rally into a bull market — defined as a 20% gain from the most recent trough.

All that is making investors fearful of calling a turning point, even though the small-cap index is hovering near the cheapest valuations since 2007 relative to the S&P 500 Index.

“You can rent the small-cap rally, but don’t own them yet,” said Manish Kabra, head of US equity strategy at Societe Generale SA. “The biggest issue is the upcoming refinancing cycle, as a quarter of firms have been loss-making in the last three years despite super-strong nominal GDP growth.”

US small caps do tend to outperform the broader market between the last Fed rate hike and its first cut. But what’s different this time is that the US rate-hike cycle has been the most powerful since the 1980s. It’s feeding into the economy, just as companies face repaying debt they gorged on during the cheap-money years.

And even before recession hits, 40% of Russell 2000 companies are loss-making, data from Apollo Global Management showed.

Debt costs are going to be problematic for companies more broadly, of course — Bloomberg Intelligence estimates corporates that borrowed in dollars may incur an extra $27 billion in interest costs when they refinance debt maturing between 2024 and 2026.

But headwinds could be magnified for small firms as they tend to carry more leverage. US small caps have more than two-thirds of their debt coming due in the next five years, compared with less than half for the S&P 500, according to data compiled by Bloomberg.

That’s enough reason to shun small caps, Peter Garnry, head of equity strategy at Saxo Bank AS, said, noting that “higher rates for longer and, potentially, a slowdown in the economy are key risks that hit these small cap companies harder than large caps.”

Small-cap fund managers are banking on an extreme discount in share prices relative to earnings to drive a rebound. Valuations are “beyond cheap” according to Nicholas Galluccio, portfolio manager of the Teton Westwood Small Cap Equity Fund. “If we’re going into a slowing economy, small caps are already predicting a recession. So the valuation gap between small and large caps will begin to close,” he added.

Such bets have lured nearly $1.7 billion to US small-cap funds so far in November, EPFR Global data showed, the first inflow in four months. And history bodes well — since the late-1980s, US small caps have typically gained 16.5% in the average of nine months between the last rate hike and the first cut, according to CFRA Research. The S&P 500, meanwhile, has risen 13.2%.

Technical Hurdle

A fair-value model based on consensus rate and macro forecasts does imply a roughly 20% upside for the Russell 2000 of US small caps, according to Bloomberg Intelligence strategists Michael Casper and Gina Martin Adams. But even that gain would leave the index short of a record high hit in 2021.

“For the small-cap gauge to break out of that range, the economy would have to re-accelerate — but with such a surge likely met by higher interest rates, the model indicates that upside in the most bullish scenario could be capped below former all-time highs,” the strategists wrote in a note.

Market technicals also indicate the rebound is running out of steam as an ETF tracking US small caps has failed to snap a longer-term downtrend channel relative to the S&P 500.

John Leiper, chief investment officer at Titan Asset Management, said a break in that ratio would mark a decisive shift in investor sentiment.

Until then, Leiper sees safety in the so-called Magnificent Seven technology behemoths, which have led US equity gains this year, as he expects weaker profits and falling sales projections for small caps.

“The bar is high and the burden of proof is on the small caps,” Leiper said.

--With assistance from Jan-Patrick Barnert.