Investors across Asia earmarked China’s ballooning levels of municipal borrowing as the region’s number one financial risk this year in a survey that ranked their biggest concerns.

China local government financing vehicles, or LGFVs, were the most frequently cited top risk in a Bloomberg survey of 53 economists, money managers and strategists at financial institutions ranging from sovereign wealth funds to banks and pensions.

Frontier market sovereign debt loads also featured among the most elevated risks for Asia, followed by mortgage-backed bonds and loans, according to the survey conducted May 9-15. Japan’s banks were the subject of lively debate as their piles of developed-market debt left some investors nervous on the outlook.

The poll offers a snapshot of the asset classes and geographies occupying the minds of financial market players tasked with navigating the world’s vulnerabilities. As the global economy sputters and markets bet interest rates are nearing the peak of the current cycle, the weak links flagged show where ructions may occur during the remainder of this year.

Other worries stemming from outside Asia such as the potential for further interest rate hikes by the Federal Reserve and ongoing wrangling over the US debt ceiling also featured heavily on radars of the survey respondents.

Here’s an in-depth look at some of the main risks highlighted in the poll, with some accompanying key metrics to monitor:

LGFVs

With a slew of data showing China’s economic rebound is faltering, focus is once again turning to troubled spots in the world’s second largest economy. In one recent example, a last minute bond payment by a local government owned firm highlighted weakening debt serviceability that’s threatening to extend worries beyond the country’s credit traders and into other markets.

The vehicles are a key method of funding China’s public infrastructure as well as its property market. S&P Global Ratings put the total debt of LGFVs at more than 46 trillion yuan ($6.5 trillion) at the end of last year. Of that, onshore bonds due in 2023 are at a record high at about 4.3 trillion yuan. Goldman Sachs Group Inc. estimates China’s total government debt is about $23 trillion, a figure that includes the hidden borrowing of thousands of financing companies set up by provinces, cities and state policy banks.

“We believe any hawkishness by Beijing on local debt would intensify the financial vulnerabilities of local governments, jeopardizing the budding economic recovery,” said Carl Liu, economist at KGI Securities in Taipei. “We think LGFVs’ debt-servicing ability is weak, and it seems that LGFVs rely on new financing to service debt, strengthening the default risk.”

Debt repayment pressure has mounted in recent years as the average bond tenor shortened. The number of missed payment cases this year is expected to exceed that of previous years as the pandemic served to squeeze some local governments’ financial resources.

The struggle for many LGFV’s is already being captured in bond markets. The financing cost of LGFVs in provinces from Guizhou to Guangxi and Yunnan had an average coupon in 2022 above 5%, reflecting their troubles raising money from capital markets, according to Laura Li, an analyst at S&P Global Ratings.

The worry is that defaults of shadow bank instruments could lead to souring of publicly traded bonds, creating financial risks that weigh on an already sluggish economy further down the line.

Mortgage-Backed Bonds

Strains have been spreading globally in real estate-related debt. The widening gap between property debt trading at distressed prices and other sectors is among key metrics to monitor. But perhaps no region in the world has experienced more upheaval with borrowings backing the sector than Asia.

Some signs were showing long before the market for mortgage-backed securities was shaken by failures of banks in the US including Silicon Valley Bank, after which the government hired BlackRock Inc. to sell the collapsed lenders’ securities.

In China, a property debt crisis has kept the mortgage-backed debt issuance market effectively shut for almost a year and a half. There have been no sales of residential mortgage-backed securities in yuan since February 2022, one of the longest dry spells on record.

And in Australia, a hawkish outlook for rates after the central bank’s hike in May could lead to a rise in arrears on residential mortgage-backed securities there, Bloomberg Intelligence analysts wrote in a recent report. “Loans originated during 2020-22 contain more risk as interest rates now exceed sensitized levels at approval.”

“Mortgage-backed bonds and loans will pose a major financial risk to the region, given growing housing market stress stemming from the impact of rising mortgage rates,” said Lloyd Chan, economist at Oxford Economics in Singapore, who chose the topic as his top risk. “Vulnerabilities will likely be acute in economies with highly leveraged households and property developers” and where house prices are declining.

Frontier Market Debt

Investors in frontier markets face a heightened risk of currency devaluations and sovereign defaults as the rising cost of importing fuel and other essential items in past years drained the nations’ foreign-exchange reserves. Ballooning debt levels as a proportion of a country’s gross domestic product are among one useful metric to monitor.

There are 16 emerging markets around the world with sovereign dollar debt that trades at distressed levels — yields more than 10 percentage points above that of similar-maturity Treasuries, which can indicate investors believe a default is a real possibility. Many of those include small frontier markets.

Pakistan has been negotiating with the International Monetary Fund to restart its $6.7 billion bailout to avert a default. Authorities are focusing on the restoration of foreign-exchange market functioning, the passage of a fiscal year 2024 budget consistent with program goals and adequate financing. Columbia Threadneedle Investments estimates the nation faces about $22 billion of external debt service for the fiscal year starting in July, about five times its reserves.

There’s also Laos. Natixis SA estimates its net external payment this year will surge more than 12 times to $600 million. That’s equivalent to about 55% of its reserves, among the highest ratios for Asian frontier nations. Meantime, in Bangladesh, Moody’s Investors Service cut the nation’s credit rating earlier this week as reserves dwindle.

The impact on investors can linger long after defaults. BlackRock and Pacific Investment Management Co., among those who suffered losses from defaults in Sri Lanka in 2022, have argued that domestic debt holders should share billions of dollars of those losses.

Project Finance

South Korea’s real estate project-finance, used to fund the nation’s construction boom, was at the heart of South Korea’s debt crisis last year after a local government-backed developer unexpectedly missed a debt payment. While the nation’s bond market has stabilized after authorities pledged billions of dollars in support last year, some strains linger in the face of a depressed property market that’s seen a surge in unsold housing inventories and a decline in home prices.

Korean banks and other financial firms have about 140 trillion won ($108 billion) of exposure to project-financing loans as of September, according to the Bank of Korea, one key metric to watch. Underscoring the strains in the industry, securities firms’ delinquency ratio on such loans surged by 2.22 percentage points from the previous quarter to 10.38% at the end of last year, compared with a 0.33 percentage point increase to 1.19% for overall financial institutions.

Korea is taking steps to accelerate restructuring of troubled assets that involve project financing. A group of about 3,000 financial firms involved in such projects signed an agreement in April on swift debt restructuring steps. The slump in the property market may lead to more defaults on project-financing loans and a collapse of any big financial institution or construction company would lead to a systematic problem on the economy and financial markets, the nation’s financial watchdog chief has said.

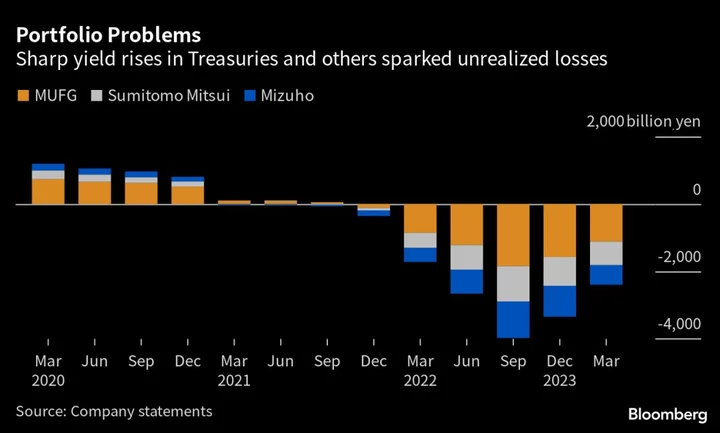

Japan Banks

Risks at Japanese banks have come into focus since the collapse of several US regional lenders and emergency rescue of Credit Suisse Group AG earlier this year. Japanese lenders are big investors in foreign bonds, which have plunged as central banks around the world hike interest rates to combat inflation.

The nation’s three largest banks are sitting on paper losses of 2.4 trillion yen ($17.3 billion) on their foreign bond holdings as of March. That’s down from the previous three months, and the Bank of Japan says banks have become more resilient to risks of higher rates as they rebalance their asset portfolios. Higher rates are also boosting their margins on overseas loans. Still, one key risk is that under a scenario where the Fed needs to keep rates higher for longer to combat inflation, this stress may spill over if these unrealized losses start to spiral.

Stress in the global financial sector may also hurt shareholder returns. Mitsubishi UFJ Financial Group Inc. and Sumitomo Mitsui Financial Group Inc. – Japan’s two biggest banks — said in May that they will hold off buying back shares for now, even after forecasting bumper profits this fiscal year.

Meanwhile, Japanese banks face the opposite problem at home, where interest rates remain close to zero. New BOJ Governor Kazuo Ueda has signaled he is not in a hurry to end the negative-rate policy, meaning domestic lending profitability is likely to remain low. That’s a blow especially for smaller regional lenders, which have fewer resources to expand abroad.

--With assistance from Richard Henderson, David Ramli, Jing Zhao, Taiga Uranaka, Karl Lester M. Yap, Richard Frost, Russell Ward, Georgina McKay, Andrew Monahan and Yuling Yang.

Author: Amy Bainbridge, Cynthia Li and Kyungji Cho