Hedge funds looking to profit from dislocations in the US Treasury market appear to be playing with the very fire that burned them so spectacularly in the depths of the pandemic turmoil.

A recent surge in leveraged positions betting that Treasury futures will fall — at a time when Wall Street is increasingly confident that a US recession will soon spur rapid central bank interest-rate cuts — smacks of so-called basis trading, market watchers say. That’s when hedge funds seek to profit from a mismatch in pricing between Treasury futures and the deliverable note or bond.

The trade usually earns tiny nominal returns, so funds use cash borrowed from the repurchase agreement market to leverage up positions and juice their wagers. The worry is that this is the same strategy that heaped steep losses on investors in March 2020, drying up liquidity not just in Treasuries but also in other money markets key to the smooth functioning of the financial system.

Here are some charts that illustrate the concerns:

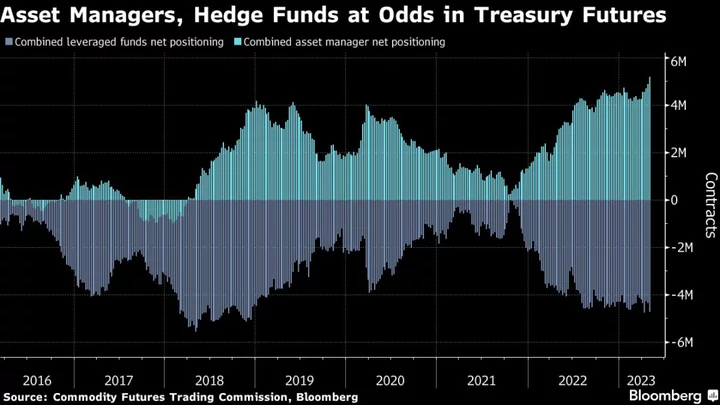

The current environment favors buying the cash bonds and selling futures against them, thanks to strong asset-manager demand for the derivatives and an increased public supply of Treasury securities as the Federal Reserve sheds its holdings.

This kind of basis trading can distort how speculators respond to economic data, making it harder for other investors to read signals from the bond market as a guide to the US outlook.

And the net short positions being held by hedge funds across most Treasury futures tenors are only continuing to grow. Data released Friday by the Commodity Futures Trading Commission for the period to May 9 showed that across the 2-, 5-, 10-, ultra-10 and ultra-long contracts combined, they had added almost $13 million per basis point in cash risk to their net short.

Adding to concern is the fact that general trading conditions are poorer now than back in March 2020.

A Bloomberg gauge of Treasury-market illiquidity has been hovering near levels last seen at the peak of the pandemic for the better part of the past year.

The one thing that is clear is that wagers on Treasury futures are near the highest they’ve ever been — indeed open interest in the pivotal five-year futures is at a record.

Despite the haven appeal of Treasuries, the recent tumult in the US banking system showed just how painful getting caught wrong-footed on rates can be.

--With assistance from Edward Bolingbroke.

(Updates with fresh CFTC data.)