Three Japanese market veterans ruminating over beer in Tokyo whether Chinese debt is the deal of the century or the road to ruin sum up the dilemma global investors face in deciding to play in the world’s second-largest bond market.

Akira Takei, Tatsuya Higuchi and Hideo Shimomura manage money for three fund management firms in the Japanese capital with a combined $640 billion in assets. While they’ve been friends for at least a decade and share interests including talking finance over drinks, their take on trading China bonds couldn’t be more diametrically opposed.

Higuchi, a three-decade finance veteran at Mitsubishi UFJ Kokusai Asset Management Co., sees China as the top destination for bond investors as interest rates climb ever higher almost everywhere.

Takei, who spent 37 years investing in sovereign bonds and is now with Asset Management One Co., wouldn’t touch China’s debt. His thesis: the securities are simply too risky to own. Fivestar Asset Management Co.’s Shimomura, who’s invested across markets over the past three decades, agrees.

“Never in my entire career” have I invested in China bonds, said Takei, who cites the nation’s property woes, capital controls and heightened geopolitical tensions with the West among the reasons. “If we invest in Chinese government bonds, there is a chance that we cannot get back that money.”

Higuchi has fewer qualms. “The slowdown of the economy is much faster than the other countries in the world, so there is a return with investing in CGBs,” Higuchi said from his office at Yurakucho, about a mile away from Takei’s at Marunouchi. “We couldn’t find any market with more than 2%” yields and a “steeper yield curve.”

China Dilemma

Their approach underscores one of the biggest quandaries in global finance: how to invest in a market that’s too large to ignore, yet vulnerable to both unpredictable Communist Party decision-making that’s brought some of China’s biggest corporate titans to heel and the geopolitical rivalry between the world’s two largest economies.

President Xi Jinping’s government has sought to curb “disorderly capital” at home even as it opens up the nation’s multi-trillion dollar markets to the world, showcasing how four decades of marrying communism and capitalism is still an unstable recipe. Heightened US-China tensions over everything from artificial intelligence to military technology to the fate of Taiwan only add fuel to this mix.

In turn, Japanese investors have much to offer China. Home to the last bastion of ultra-low rates, they have already unleashed a $4.2 trillion firehose of cash on the investment world and are hungry to buy assets offering the chance of higher income. The question is just how much risk they’re willing to take in order to secure those returns.

Investors in China have been burned before, even in bonds. A Bloomberg gauge of the country’s government debt fell 5% last year and about the same in 2016, in dollar terms. And China’s shock devaluation of the yuan in 2015 is still much discussed in markets, especially with the currency back under pressure.

While China’s bonds have outperformed their global peers in recent years, that hasn’t stopped foreign investors from exiting the market – last year’s outflows hit a record 616 billion yuan ($86.3 billion). They have only just begun a tentative return.

For Fivestar’s Shimomura, China’s price tag is currently too high to pay.

“I don’t think we would want to enter now due to factors ranging from regulatory issues surrounding their bond market, a not-completely-free market overall,” said Shimomura. “I do not hold a bullish view on China nor do I plan to invest for now.”

To counter a view like that, Beijing has been ramping up efforts to lure more foreign players to its shores. It introduced Swap Connect, a trading link that grants offshore investors access to onshore interest rate swaps earlier this year and opened up trading for futures on 30-year government debt, providing a new hedging mechanism for longer-dated bonds.

China also signaled that it may grant global investors wider access to the repo market, a crucial funding tool.

Top Performers

All of this bolsters the case that avoiding the country’s markets now may be costly.

While China’s re-opening after the pandemic has been lackluster, that has spurred additional stimulus and monetary policy easing measures to reboot the $18 trillion economy. The latest came when China’s Politburo of top leaders on Monday pledged to boost consumption and offer more support for the troubled property sector.

China’s government bonds have gained more than 3% this year, beating a near 2% rise in a global debt gauge, according to data compiled by Bloomberg. The yield on China’s 10-year bond was trading around 2.65% on Wednesday.

What Bloomberg Strategists Say...

“The People’s Bank of China may unleash all monetary tools in 2H to safeguard the increasingly concerning macro recovery, which include cutting policy rates and required-reserve ratio (RRR) further, and also expanding on the structural policy tools.”

- Stephen Chiu, chief Asia FX & rates strategist. For the full note, click here

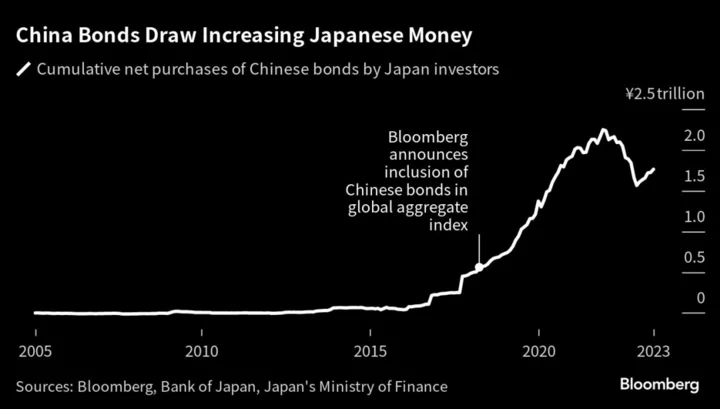

Japanese inflows to China’s bond market have increased in the last six years, with demand underpinned by the securities’ inclusion in global benchmarks such as Bloomberg’s Global Aggregate Index and FTSE Russell’s World Government Bond Index. Still cumulative purchases since 2005 have totaled just 1.76 trillion yen ($12.5 billion), or a mere 2% of those for US debt, according to Japan’s balance-of-payments data.

“Chinese government bonds, overall, are very good to invest in because their yields might go down further,” said Higuchi. It is “much easier to have duration risk in the Chinese bond market.”

Benchmark 10-year government debt yield and 5-year equivalent both fell about 18 basis points this year to 2.66% and 2.46%, respectively.

Takei though is comfortable sacrificing performance if it means he’s protecting his portfolio. He’s particularly wary of the nation’s property market that has seen a proliferation of debt blow-ups along with “zombie companies” that have been propped up by authorities.

“It’s very hard to envisage where the robust economy is coming from in China, especially in relation to debt,” he said.

(Updates with China bond yield. A previous version corrected the spelling of office location in the sixth paragraph.)

Author: Ruth Carson, Masaki Kondo and Yumi Teso