The UK’s sale of ultra-long gilts this week will offer the highest coupon in almost 15 years, a sign of the elevated funding costs that governments must now bear.

The 40-year conventional bond will pay 4%, reflecting the jump in yields after more than a year of interest-rate hikes. But it may have to offer an additional concession to lure a key part of the buyer base.

Investors say the bond will need to price at a discount — below par — to attract pension funds pursuing liability-driven investment strategies, who prefer lower coupons due to their higher duration — market parlance for interest-rate sensitivity.

If priced correctly, money managers say the offer could go as well as a recent inflation-linked sale that drew record demand.

“The success of the long-dated index linked bond syndication at the end of April showed that the LDI market is alive and well,” said Robert Scammell, senior portfolio manager at Van Lanschot Kempen, who is considering buying the notes. “There is no reason to think that the nominal bond on offer, providing it is priced appropriately, would not continue the trend.”

Another successful sale would show how the UK government is managing to raise funds for a budget laden with crisis spending, even as it comes just days after the Bank of England lifted rates to 4.5% and left the door open to further tightening. The Debt Management Office is planning to sell £237.8 billion ($296 billion) of gilts in the fiscal year 2023 to 2024.

Pension funds were at the center of the gilts crisis in September, forced to dump their holdings amid the fallout from former Prime Minister Liz Truss’s announcement of unfunded tax cuts. While they’re not the only investors to buy these ultra-long securities, their participation is particularly important in such a supply-heavy year.

Britain’s financial services watchdog has since implemented a series of reforms to amend shortcomings in the risk management of LDI investment strategies. That regulatory clarity should encourage fresh buying by those funds, according to Daniela Russell, head of UK rates strategy at HSBC Bank Plc.

“Many are likely to see the syndication as a key point of improved liquidity,” she said. “With long-end yields above 4% — and likely to move lower as we move through the year – current valuations provide an attractive level at which schemes can de-risk.”

UK Regulators Want LDI Pensions to Be Ready for Future Bond Rout

BOE data also point to healthy demand for gilts: domestic buyers bought a record number in the first quarter of the year, despite policymakers’ ongoing battle with inflation still at the highest among developed markets.

A surprisingly resilient UK economy has paved the way for additional interest-rate hikes, pushing terminal rate pricing to around 5% later this year, according to money-market wagers.

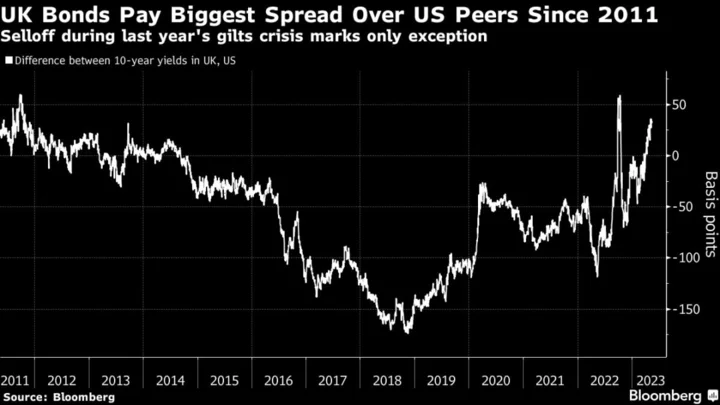

Gilts have fared poorly relative to other markets against that backdrop.

UK 10-year bonds are poised to lose out to their US equivalents for a record seventh month. The extra yield investors demand to hold UK bonds compared with similar-maturity German ones is increasing for a fourth month, the longest streak since October 2020.

The question now is when investors should jump in without getting stuck with a depreciating bond if rates go even higher.

Ian Fishwick, a fixed income portfolio manager at Fidelity International, said markets are still weighing flagging growth against still-stubborn inflation. The UK economy shrank unexpectedly in March, which seemingly runs counter to the BOE’s biggest upgrade to growth projections in a quarter century.

“We would like to go a bit longer in terms of absolute duration,” said Fishwick. “However, as we don’t know where rates will peak, it is hard to gauge what the correct downward slope on the curve should be and therefore we are currently neutral on duration.”

Columbia Threadneedle Investments and Aviva Investors see UK bonds recovering as the economic blow from a combined 4.4 percentage points of interest-rate hikes makes itself felt and hastens a drop in the inflation rate.

“The BOE should have plenty of scope to conclude they’ve done enough tightening” by its next meeting, said Alexander Batten, fixed income portfolio manager at Columbia Threadneedle. He expects inflation to be closer to 7% by that point compared with more than 10% now.

BOE Chief Economist Says UK Inflation at ‘Turning Point’

The more the BOE hikes, the larger and quicker the cuts when they come, said Ed Hutchings, head of rates at Aviva Investors. He’s long gilts on a cross-market basis and sees yields supported over the medium term.

“The headwinds are going to start to hit,” he said.

Author: Alice Gledhill, James Hirai and Naomi Tajitsu