A Florida state agency is selling municipal bonds to backstop the state’s homeowner’s insurance industry after a surge of claims and litigation drove some insurers to shutter.

The Florida Insurance Guaranty Association, which handles the claims of insolvent insurers, plans to borrow $600 million of bonds, according to preliminary offering documents. It is the first time in three decades the agency has tapped the municipal bond market to help support insurance claims.

The borrowing provides the agency with needed liquidity. “Our funding sources are somewhat limited,” said Corey Neal, FIGA’s executive director.

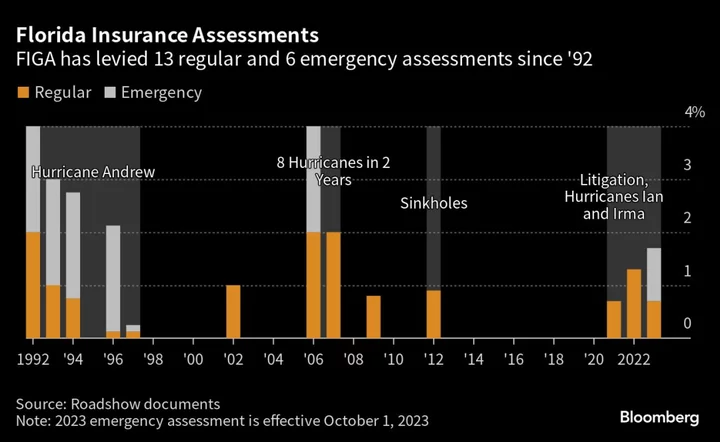

Historically, the agency has used investment income and the assets of liquidated companies to cover payouts. The last time FIGA sold a muni bond for such purposes was in 1993 after Hurricane Andrew devastated South Florida, causing an estimated $27 billion in damages.

An uptick in insurance claims after last year’s Hurricane Ian and a deluge of lawsuits forced 10 property insurers to close since 2019, according to roadshow documents, pushing the agency’s costs higher.

Related: Rebuilding Florida Cities Face Highest Borrowing Costs in Decade

Pullback among larger, national insurers in the state has concentrated exposure to smaller, more local firms. Farmers Insurance Group, for instance, no longer offers homeowners policies in Florida, and Nationwide has already paid out its full year’s budget for storm damage, according to a research note by Municipal Market Analytics.

“They’re not making enough profit,” said Neal, referring to insurers. “Some companies don’t have an appetite for Florida because it’s more risk.”

Since 2019, 10 property insurers that collectively wrote over 440,000 policies in Florida have been declared insolvent, amounting to a net cost to FIGA of about $1.6 billion, according to bond documents. Rampant litigation and fraud, rather than storm damage, have been the primary drivers of their collapses, the documents said. In 2021, Florida represented just 6.9% of total homeowner’s claims, but 76% of the nation’s homeowner’s lawsuits.

The bonds, which are being sold in multiple series through the Florida Insurance Assistance Interlocal Agency, are backed by a 1% emergency assessment levied by the state’s Office of Insurance Regulation, similar to a tax on a range of insurance policies. The average premium in the state is about $4,200 on a roughly $350,000 home, so the assessment translates to about $42 a year, Neal said.

That levy is expected to generate $286 million annually, according to bond documents. FIGA currently has authority to levy as much as 4% of emergency assessments, and 2% of regular assessments.

“They are really stepping up to try to find solutions,” said John Meder, head of risk consulting and claims advocacy at Risk Strategies.

Bank of America Corp. is managing the deal which is slated to price on June 27, the documents said.

Given that Florida investors are familiar with similar structures backstopping insurance, the sale is expected to be well-received. In 2020, Florida’s State Board of Administration Finance Corp. seized on low-interest rates to borrow $3.5 billion for its catastrophe insurance fund, which functions like public reinsurance for member companies.

Related: Florida Boosts Hurricane Fund Debt Sale by 56% to $3.5 Billion

That reason coupled with it being summer, a typically strong season for munis, “I wouldn’t be surprised if this deal does pretty well,” said Jason Appleson, head of municipal bonds at PGIM Fixed Income.

--With assistance from Max Reyes.