A pair of bond sales in the past week shows how European governments are increasingly turning to households to tackle the challenges of a high interest-rate landscape.

If they gauge it right, countries like Belgium can offer an interest rate that’s appealing to its citizens while lowering sovereign borrowing costs, in what Société Générale SA analysts call a “win-win.” The nation has already attracted over €22 billion ($24 billion) for the note, with the final results due Monday.

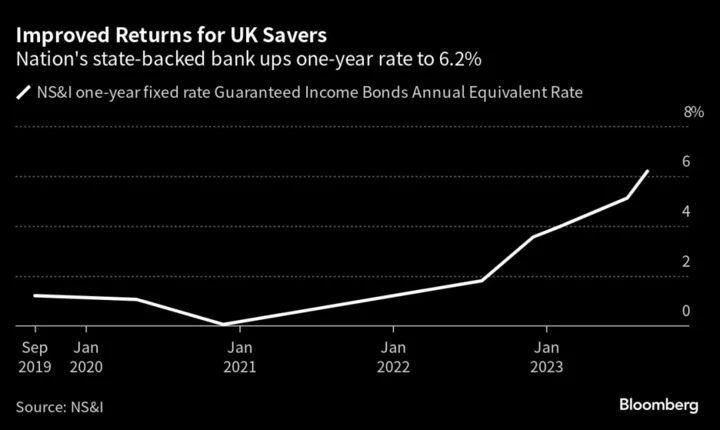

The sales also encourage lenders to offer their customers higher interest on deposits. That’s key in the UK, where a bond boasting a yield far above the prevailing market rate was sold to Brits this week, increasing competition and getting banks to more fully reflect recent central bank rate hikes.

“There’s a lot of pandemic savings, but a lot of is still out there because it’s been held by these wealthier members of society,” said Richard McGuire, head of rates strategy at Rabobank, in a phone interview. “This is something governments in Italy, Portugal and now Belgium have cottoned onto.”

Belgium’s sale of one-year notes dwarfs the debt agency’s €250 million retail-bond target for this year and should help keep a lid on the yield of some of the nation’s other debt, according to analysts at SocGen and Rabobank.

Europeans are relieved to see the back of zero and even negative rates and the sales show there’s lots of appetite among ordinary citizens for higher-paying products. Governments are looking to diversify their funding base as they face higher financing costs and growing spending plans.

Some nations have proved more willing to tap their citizens savings than others.

Italy has an established and innovative retail-bond market. Its so-called BTP Futura range, first sold in 2020, links returns to economic growth. And in June, the nation sold BTP Valore debt, which comes with a bonus payment for holding until maturity. The government raised more than €18 billion from that sale, a record amount for an Italian offering pitched at retail investors.

After household demand surged in Portugal, the government cut back its planned issuance of bonds and bills to institutional investors by almost €9 billion.

The jumbo sale in Belgium harks back to a blowout retail offering in 2011 when it raised €5.7 billion. Belgium had put its retail program on ice for three years before tiptoeing back into the market with smaller issues since 2022.

The latest sale means the government can afford to cut sales of its bills and bonds aimed at institutional investors.

“With European government bond yields of all maturities continuing to climb, domestic retail investors have been keen to buy the dip,” said Société Générale strategist Sean Kou. Kou’s team recommends buying the nation’s bills versus equivalent French securities on a bet the “extraordinary demand” for its retail bonds sees Belgium reduce its short-maturity borrowing program.

Political Pressure

In many countries, banks have been slow to raise interest rates because they’re still flush with cash after years of monetary stimulus. But political pressure is rising.

Belgium said its sales were intended to encourage commercial lenders to up their offerings, while UK regulators and lawmakers have lambasted banks for their stingy savings rate. Austria plans to offer retail government bonds via direct sales to households seeking alternatives to low-rate bank deposits, Finance Minister Magnus Brunner said Aug. 23.

The UK’s state-backed savings bank, known as NS&I, released a new one-year note at the end of the month that pays 6.2% — well above the market average.

“I suspect there was an element of leaning on the NS&I to come out with a competitive savings product, in order to keep pressure on the high street banks to pass through BOE policy rate hikes,” said Aaron Rock, an investment director at abrdn.

To be sure, household demand is a fraction of the firepower wielded by institutional investors. Maturities are another limiting factor. Belgium’s latest blockbuster comes due in just one year, a tenor that will ultimately limit its impact on spreads, according to Ronald van Steenweghen, an investor at Brussels-based Degroof Petercam Asset Management.

Still, the placement confirms that Belgian savers have a lot of confidence in the government, which could be seen as a positive for bonds more broadly, he said.

For Rabobank’s McGuire, Belgium’s success on the heels of Italian and Portuguese retail offerings might encourage others nations to follow suit.

He suggests the Netherlands could be next to tap the “retail reservoir,” citing the nation’s large household savings and the appeal of Dutch bond yields compared with interest rates on commercial deposits.

--With assistance from James Hirai, Alice Gledhill and Lyubov Pronina.