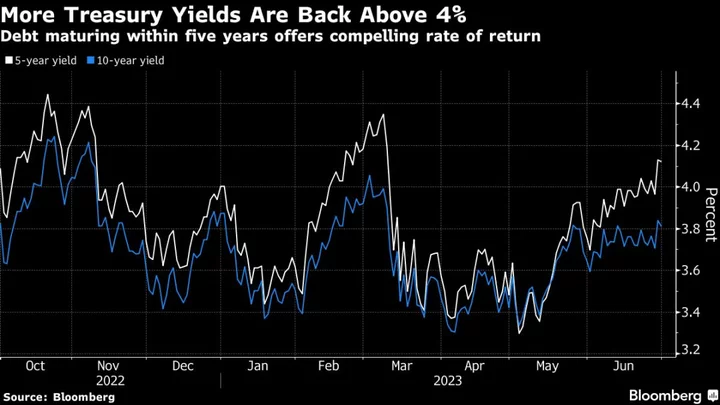

Bond traders are bracing for another tumultuous week in which key employment data could push yields on 10-year Treasuries toward 4%, a level that market watchers see luring investors into government debt.

The benchmark US rate rose to within striking distance on Thursday, climbing as high as 3.89%, after an upward revision to first-quarter US economic growth and a drop in initial jobless claims sparked the biggest day for Treasuries in more than three months. Yields for most tenors approached the highest levels seen so far this year, while wagers that the Federal Reserve might cut interest rates this year fizzled.

A wealth of events next week could unleash fresh bouts of selling and lift yields to 4%, not least the release of the first major economic reports for June — including key labor-market data — as well as minutes from the Federal Reserve’s latest meeting. But for bond investors, the question is now whether yields in the 4% neighborhood are attractive, and whether they offer sufficient compensation for the risk that the central bank will fail to get inflation under control.

The 4% level for 10-year yields “will bring in a wave of demand” from investors, said Zachary Griffiths, senior fixed-income strategist at CreditSights Inc.

The research firm sees a 50-50 chance of one additional Fed rate increase at the next policy meeting concluding July 26 — and quarter-point cuts at each meeting in 2024. Even if that scenario doesn’t play out and the Fed is more aggressive, Griffiths sees that limiting any selloff in longer-dated Treasuries.

On the other hand, interest-rate strategists at JPMorgan Chase & Co. ditched their bullish call on Treasuries this week in anticipation of additional cheapening, and Bill Dudley — a former president of Fed’s New York bank — said 4.5% was “a conservative estimate” for the peak in 10-year yields.

It all hangs on how many hikes it takes for the Fed to get a handle on inflation, and whether they can do so without pushing the economy into a painful recession.

The Fed left its policy rate unchanged at 5%-5.25% on June 14 after 10 consecutive increases, as most forecasters expected. Revised quarterly forecasts for the economy and monetary policy released that day showed officials expect to raise rates twice more by year-end.

Minutes of the June meeting are slated to be released on Wednesday and may clarify the rationale for the pause, which Fed Chair Jerome Powell has said was appropriate to assess how elevated policy rates are impacting the economy. Signs of trouble appeared in March when several regional banks failed because of losses on their securities holdings related to higher borrowing costs, but other indicators — such as those focused on employment — remain robust.

“The market is very focused on the labor markets as the thing that needs to break weaker to finally get the Fed to be truly done for the cycle,” said Dominic Konstam, head of macro strategy at Mizuho Securities. Central banks “are clearly fearful that policy isn’t sufficiently restrictive to curb inflation.”

Still, the expectation that the Fed tightening cycle is sowing the seeds of lower inflation helped drive long-maturity Treasury yields toward historic lows relative to shorter-maturity ones this week. The two-year yield exceeded the 10-year by nearly 107 basis points, within 4 basis points of the biggest gap in decades.

Breakeven inflation rates for Treasury Inflation-Protected Securities — the average annual inflation rates needed to equal the higher returns from regular Treasuries — have nearly returned to the sub-2% levels that prevailed until 2021. Five- and 10-year breakeven rates are around 2.2%, compared with the 4% year-on-year rate for the consumer price index in May.

And JPMorgan’s weekly Treasury client survey this week found the highest level of positive sentiment in more than a decade.

“The tightening cycle will catch up with the economy,” said Laird Landmann, co-director of fixed income at TCW Group Inc. “A couple more rises in the funds rate means we get to a point of more accidents, and that will bring a slowdown in the US economy or a hard landing.”

For institutional investors such as endowments and pension funds, Treasury yields are currently attractive, Landmann said.

What to Watch

- Economic data calendar

- July 3: S&P Global US manufacturing PMI; ISM manufacturing; construction spending

- July 5: Factory orders

- July 6: MBA mortgage applications; Challenger job cuts; ADP employment; trade balance; weekly jobless claims; S&P Global US services PMI; Jolts job openings; ISM services index

- July 7: US employment report for June

- Federal Reserve calendar:

- July 5: FOMC meeting minutes from June 13-14; New York Fed President John Williams

- July 6: Dallas Fed President Lorie Logan

- Treasury auction calendar:

- July 3: 13- and 26-week bills; 42-day cash management bills

- July 5: 17-week bills

- July 6: Four- and eight-week bills