Bond investors are coalescing around a segment of the Treasuries market that offers a measure of protection from this year’s brutal rout and also positions them for the recession that some still anticipate.

BlackRock Inc. and Columbia Threadneedle Investments are among firms favoring notes due in roughly one to five years as Treasuries head for a record third straight annual decline, led by losses in longer maturities. Those tenors in particular have been buffeted by a resilient economy and the government’s swelling borrowing needs.

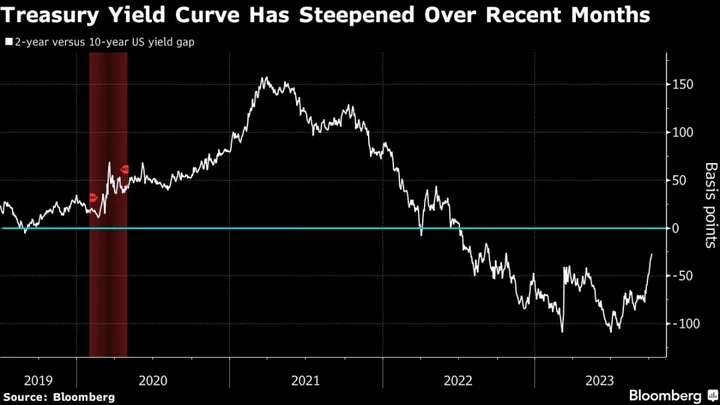

Treasuries slumped a fifth consecutive week after hotter-than-forecast US payrolls data on Friday boosted expectations that the Federal Reserve will raise interest rates again this year. Ten- and 30-year yields reached the highest since 2007, extending the massive resteepening of the yield curve that’s been a key dynamic of the past month’s abrupt selloff. It’s the kind of shift in the curve that’s tended to precede a recession in the past.

The jobs data may highlight the economy’s strength now, but some market watchers see it raising the risks down the road as the Fed holds rates higher for longer. Surging long-term yields are adding to the headwinds to US output, which is already facing a hit from the resumption of student loan payments and a strike by autoworkers.

“It is most likely that growth is being mispriced next year,” said Ed Al-Hussainy, a global rates strategist at Columbia Threadneedle. “You can say people have positioned for a recession prematurely and have been burnt, but you can only look forward, and today you are seeing rates now discounting very elevated real and nominal rates well into the future.”

The firm prefers 3- to 5-year Treasuries because “if the data weakens, rates will rally.”

Treasuries are down 2.2% this year through Oct. 5, after losing an unprecedented 12.5% last year and 2.3% in 2021, Bloomberg index data show. Amid the slide, long bonds have suffered historic losses.

Read more: Long Bonds’ Historic 46% Meltdown Rivals Burst of Dot-Com Bubble

Forces including still-elevated inflation and the onslaught of Treasury supply to fund growing deficits have led investors to demand higher yields on longer-maturity debt, lifting a measure known as the term premium.

While yields across maturities have surged, shorter-dated tenors have climbed less. As a result, the spread of 2-year yields over the 10-year rate reached its slimmest since last year on Friday.

“We don’t want to buy bonds, like 30-year bonds, but the front end of the curve is really starting to get to levels that are much more attractive,” Jeffrey Rosenberg, portfolio manager of the systematic multi-strategy fund at BlackRock, said on Bloomberg Television on Friday.

What Bloomberg’s Strategists Say...

“The US yield curve should continue to steepen, with increased Treasury-bill issuance likely one of several supportive factors. In showing this, we’ll get to a deeper problem in markets analysis: the limitations of correlation.”

— Simon White, macro strategist

Click here for the full report

Investors who typically focus on T-bills are also beginning to see a reason to extend to slightly longer maturities given that the Fed is getting close to the end of its tightening cycle and the vulnerability of long-dated debt.

“Inflation is still likely to remain sticky, above the Fed’s 2% target for a while, which all bodes for more term premium to be built into the long-end of the yield curve,” said Jerome Schneider, head of short-term portfolio management and funding at Pacific Investment Management Co.

“Meanwhile, we think we are near an inflection point for Treasury bills with rates likely near a peak,” he said.

He favors extending out to the 1- to 3-year maturities, “especially as the economy is likely to continue to be slowing down into next year.”

What to Watch

- Monday, Oct. 9 is Columbus Day, a recommended holiday for the US bond market.

- Economic data calendar

- Oct. 10: NFIB small business optimism; wholesale inventories; NY Fed 1-year expectations

- Oct. 11: MBA mortgage applications; producer price index; FOMC meeting minutes

- Oct. 12: Consumer prices; real average hourly earnings; jobless claims; monthly budget statement

- Oct. 13: Import and export price index; University of Michigan sentiment

- Fed calendar

- Oct. 9: Dallas Fed President Lorie Logan; Fed Vice Chair Michael Barr; Governor Philip Jefferson

- Oct 10: New York Fed’s System Open Market Account manager, Roberto Perli; Atlanta President Raphael Bostic; Governor Christopher Waller; Minneapolis Fed President Neel Kashkari; San Francisco Fed President Mary Daly

- Oct. 11: Governor Michelle Bowman; Waller; Bostic; Boston Fed President Susan Collins

- Oct 12: Bostic; Collins

- Oct 13: Philadelphia Fed President Patrick Harker

- Auction calendar:

- Oct 10: 13- and 26-week bills; 43-day cash management bills; 3-year notes

- Oct 11: 17-week bills; 10-year notes

- Oct 12: 4- and 8-week bills; 30-year bonds