Emerging-market bulls are still upbeat on the asset class, even after China’s highly-touted reopening rally fizzled and proved Wall Street’s early 2023 optimism to be misplaced.

Developing-nation assets stand to finally take off in the second half, they say, as long as global interest rates peak, Chinese authorities prop up growth and structural reforms in India bolster sentiment. A revival may still make this the decade of emerging markets that Morgan Stanley Investment Management flagged earlier this year.

“India, Brazil, China, they don’t have an inflation problem any longer, so they may cut rates faster than the Federal Reserve,” said Xavier Baraton, global chief investment officer at HSBC Asset Management in Paris, on Bloomberg Television. “If you’re looking for true diversification at this time, you’ve got to look into true EM. You’ve got to look into Asia. You’ve got to look into India, which is under-appreciated.”

While the first half of 2023 hasn’t been a disaster for EM investors, it has fallen far short of buoyant forecasts.

MSCI Inc.’s emerging-market stock index has risen 4.8% so far this year, well behind the 11% gain in a gauge of developed-nation peers. An index of EM currencies, meantime, edged up 1.7%. And emerging local-currency bonds have only narrowly outperformed a global debt gauge.

What Bloomberg’s Strategists Say

It’s nice to see that there’s more to investment life than simply buying ludicrously-valued tech stocks, and that one can derive comparable if not superior returns from alternative strategies with a less odious value proposition. If global inflation and monetary tightening has had one positive impact from an investment perspective, it’s been the revival of the good old-fashioned EMFX carry trade.

— Cameron Crise, macro strategist

For the full column, click here

Among the factors crimping gains, China’s exit from Covid-Zero restrictions has failed to translate into broad economic strength, instead boosting spending on services such as travel and eating out, leading to weak credit growth, contracting exports and a slowdown in housing sales. The impact has spread to other markets that rely on Chinese demand such as South Africa and Thailand.

That’s cast doubt on the bullish view set out by Morgan Stanley Investment Management in January: that emerging-market stocks are set to be this decade’s winners amid attractive valuations and a superior growth outlook — especially in countries such as India.

Equity Opportunity

On the positive side, the underwhelming numbers so far mean some metrics are now identifying pockets of value across of the emerging-market landscape.

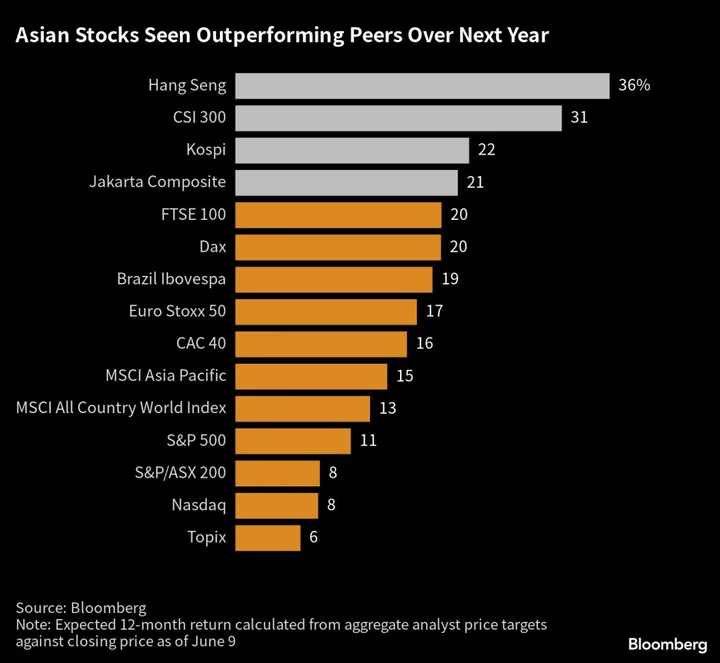

Benchmark share indexes are expected to rise in most emerging markets by year-end, with some of the biggest gains expected in Hong Kong and mainland China, according to aggregate analyst price targets compiled by Bloomberg.

“The pessimism, particularly in China and Hong Kong, has been extreme and is not accurately reflecting the economic fundamentals,” said Greg Lesko, a managing director at Deltec Asset Management LLC in New York. He favors consumer names that are likely to be supported by targeted Chinese stimulus.

“Alibaba, JD.com are silly cheap and have tons of cash, but got hit on US-China tensions,” he said. “Indonesian banks are money-making machines.”

Value in Currencies

Many emerging-market currencies may also be set to strengthen as the Fed nears the end of a tightening cycle that has already been underway for more than a year.

“Assuming that we are one or two hikes away from the peak, then that headwind to EM currency performance should dissipate,” said Edwin Gutierrez, head of emerging-market sovereign debt at abrdn Plc in London. “It also psychologically will pave the way for more EM central banks to consider rate cuts in the coming months.”

The lack of a clear driver has led to scattered performance among emerging currencies this year, while uncertainty over Fed tightening has boosted volatility. The Colombian and Mexican pesos have both surged more than 10%, while the Turkish Lira has tumbled about 20%.

The end of global rate hikes will help reduce volatility and support the carry trade, and that will benefit higher-yielding EM currencies and bonds, said Alvin T. Tan, head of emerging-market currency strategy at RBC Capital Markets in Singapore.

“A more concerted return of the carry trade would benefit the higher carry Latam and EMEA currencies even more, excepting the ones under the spell of unorthodox policies, such as the Turkish lira,” he said.

Developing-Nation Debt

There are advocates for developing-nation bonds, too, as peaking central-bank interest rates boost the attractiveness of higher-yielding assets.

“We are anticipating the start of the easing cycle out a number of emerging markets in the second half of this year, starting with the Latin American economies, and also then some of the Central and Eastern Europe economies,” said Phoenix Kalen, head of emerging-market research at Societe General SA in London.

“There is space for there to be some thinking about pre-positioning for those rate cuts, and space for the rates to come back in — especially given how high real policy rates are at this point in time, especially out of Latam,” she said.

Yield-hungry investors have already been piling into Indonesian bonds after the central bank all but ended its tightening cycle earlier this year, while its domestic coffers remain healthy from the rally in commodities. Rupiah-denominated debt has returned about 11% in dollar terms this year.

Indian bonds are also looking attractive due to good growth, a potential rate cut later this year as inflation moderates, and a trade balance that has “never been better,” said Eric Lo, Asia fixed income portfolio manager at Manulife Investment Management in Hong Kong.

What to Watch

- India is forecast to say inflation slowed for a fourth month in May. The nation’s central bank left its key rate unchanged last week

- The People’s Bank of China will review its one-year term lending facility, while the country will also release retail sales and industrial production numbers. Weaker-than-expected inflation data last week boosted expectations for a rate cut

- In Latin America, Brazil will announce retail sales for April, and Mexico will publish industrial-production numbers for the same month

- The Fed, European Central Bank and Bank of Japan all meet in the coming week, which may also influence emerging-market assets

--With assistance from Malavika Kaur Makol and Srinivasan Sivabalan.