Judging by China’s official statistics, the nation’s housing market has been remarkably resilient in the face of tepid economic growth and record defaults by developers.

New-home prices have slipped just 2.4% from a high in August 2021, government figures show, while those for existing homes have dropped 6%.

But the picture emerging from property agents and private data providers is far more dire.

These figures show existing-home prices falling at least 15% in prime neighborhoods of major metropolitan areas like Shanghai and Shenzhen, as well as in more than half of China’s tier-2 and tier-3 cities. Existing homes near Alibaba Group Holding Ltd.’s headquarters in Hangzhou have dropped about 25% from late 2021 highs, according to local agents.

While it’s difficult to make apples-to-apples comparisons, industry insiders and economists say China’s official home-price indexes are likely understating the depth of the downturn, in part because of longstanding methodologies that struggle to capture market turning points.

That’s heightening concern among investors about the availability of timely economic data in China, where access to some information has become increasingly restricted under the government of President Xi Jinping. It also raises questions about whether policy makers themselves have an accurate understanding of the market as they devise measures to prop up demand. Another risk is that wary homebuyers stay on the sidelines, waiting for price declines to show up in the data before they step in.

Analysts say the methodology, which partly relies on surveys rather than price data from transactions, helps authorities to smooth the trend and to avoid large swings. By contrast, in the US, the widely cited S&P CoreLogic Case-Shiller indexes use home-price data collected at local deed recording offices across the country.

For Henry Chin, who’s spent more than 20 years researching global real estate markets, the data’s source and accuracy are critical.

“Home-price data in many countries are based on total market transactions, yet China uses selective samples,” said Chin, the head of research for Asia Pacific at CBRE Group Inc. “When a market goes down, the true market condition is hard to be reflected in such data.”

China’s statistics bureau has said in an online explanation that raw data on new-home prices is based on all sales and purchases registered in local housing transaction bodies. Existing-home prices, though, are based on both sales of key projects and surveys, it said. The NBS uses the Laspeyres price index, a common formula used worldwide, to calculate its 70-city home-price gauge, the statistics bureau told Bloomberg. Market watchers say the methodology on sampling and index calculation remain ambiguous.

Survey-based data “serves a purpose avoiding extreme fluctuation,” said Alicia Garcia Herrero, chief Asia Pacific economist at Natixis SA in Hong Kong. “But when people are wary that prices are falling even more, thus not buying, such data defeats its own purpose.”

This partly explains why home price changes implied by official and private sources appear inconsistent with market perceptions on some occasions, Goldman Sachs Group Inc. economists said in a July report called “Understanding differences in China’s home price measures.”

Unlike in many parts of the world, Chinese authorities do not publicly disclose home prices after the transaction settles. In 2021, the statistics bureau responded to concern on the official home-price index, saying it is able to “generally” reflect changes in supply and demand in the property market, according to a statement on its website.

Price Slides

In Hangzhou, close to where Alibaba is headquartered, home prices in some neighborhoods are down 25% to 28% from a peak around October 2021, agents said. In Lianyang, a downtown area popular with expats and financiers in Shanghai, residential prices have slid 15% to 20% from record highs in mid-2021, they said.

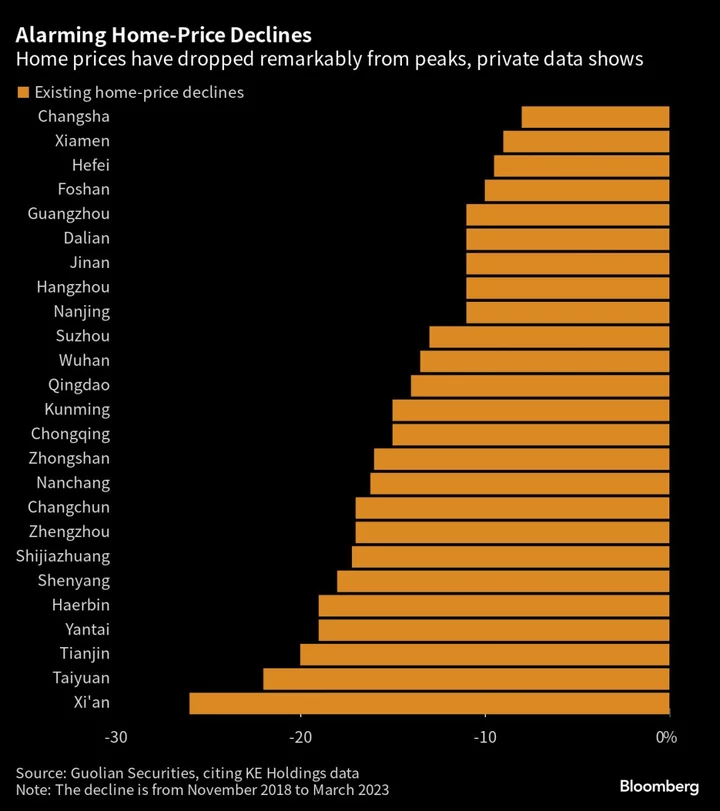

Even as of March, before a fresh slowdown, more than half of tier-2 and tier-3 cities saw existing-home prices fall more than 15% from peaks, Guolian Securities Co. economists wrote in a report citing data by existing housing transaction services provider KE Holdings Inc. Actual declines from peaks could be sharper, as the agency only compiles data starting November 2018, the economists cautioned.

Top cities, once considered resilient against a housing downturn, aren’t immune. Prices of existing homes in at least five popular districts of Shenzhen have slumped 15% in the past three years, according to a July report by property research institute Leyoujia. The southern hub is the country’s least affordable housing market.

All data sources in China, be it government or private ones, face “significant challenges” for compiling a portfolio that’s relatively stable for tracking home prices, Goldman Sachs China economists led by Wang Lisheng wrote in the July report. In their assessment of China home price measures, they said there is “no perfect” gauge.

“Property weakness is perhaps the most challenging growth headwind amid China’s ongoing post-reopening recovery, and thus the momentum and sentiment in the property sector have significant implications for growth and policies,” Wang wrote. “Home prices warrant more attention amid the tug-of-war in the property sector between persistent downward pressures and increasing easing hopes.”

The perception gap on home prices stems in part from the vast array of policy levers the authorities have at their disposal. While countries such as Australia, Singapore or the US tend to tighten loan-to-value limits or lift interest rates, China can go beyond this to ban anyone not born in a particular city from purchasing homes or limiting the number of properties a person is allowed to own.

“The weaknesses in housing price statistics hardly makes things better,” said Bert Hofman, former China country director for the World Bank who’s now at the National University of Singapore. This “may now work against determining the right policy to stabilize the market.”

First Homes

The Chinese government also intervenes on prices directly. As most new homes in China are sold before they are built, one distortion comes from a regulatory ceiling on those projects. Through a “pre-sales permit,” local housing authorities set home prices that developers intend to sell the properties for.

Since 2016, the approach successfully kept new-home prices in the biggest cities largely flat after a home-buying frenzy, even when existing-home values continued to soar. Then, when prices began falling, the arrangement helped to make new residences decline less, despite a severe slowdown.

“The price gap has become a huge disturbance to correctly reading the home market,” said Yan Yuejin, a research director at E-house China Research and Development Institute. “Some popular new projects make people feel the market is red-hot, but in reality some suburban projects are really hard to sell.”

Existing Homes

Existing home prices have also been affected by distortions in recent years, according to Goldman analysts. Since 2021, governments in more than a dozen major cities established a so-called “reference rate mechanism” for the existing-home market, substituting market-based prices with government-suggested ones to cool home-buying fever.

Besides these, there’s also a long-standing practice to create separate contracts with lower existing-home prices for tax purposes, making prices in official transactions artificially lower than real ones.

Real transaction prices are hard to come by, according to Guo, a Shanghai-based property agent who asked to be identified only by his surname discussing a sensitive matter. Transaction data often reflects the artificially low prices lodged by buyers and sellers with authorities, rather than actual transaction prices, he added.

A real estate market where the accuracy of information is questioned may hold back buyers and could mean future policy responses are harder to determine.

“Beijing has already done some things to ease the tensions in the property sector, but it has been too slow and too little,” said Lu Ting, chief China economist at Nomura Holdings Inc. “At some point in time Beijing will be compelled to take more measures to stem the downward spiral.”

--With assistance from James Mayger.