Timur Turlov is still trying to make sense of how Hindenburg Research’s bet against his Kazakh brokerage backfired so much that at one point it left him with a paper windfall of more than $1 billion.

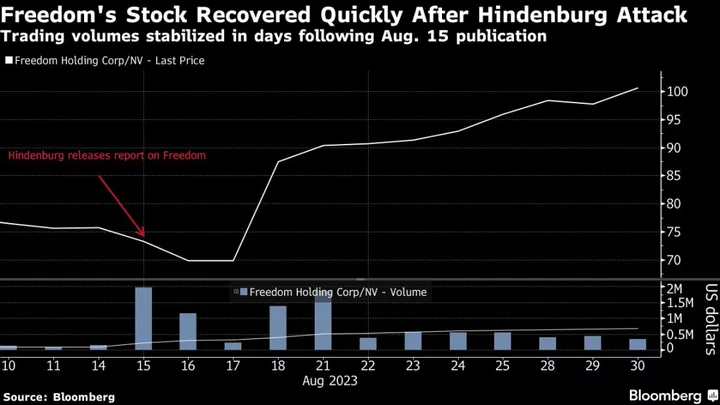

The US short seller took aim at the Kazakh billionaire’s Freedom Holding Corp. in August with accusations that ranged from fraud and market manipulation to circumventing sanctions. Days later, the company’s stock surged to a record.

The 35-year-old has emerged from the ordeal to explain for the first time how his company weathered what he describes as “a very expensive and quality lesson from Hindenburg.” Turlov controls about 71% of Freedom, a stake now valued at $3.6 billion.

As Turlov built a regional behemoth with a toehold in the US, Freedom for years had customers buy the brokerage’s own shares in exchange for access to American stock listings. The controversial tie-up was likely its best line of defense against Hindenburg.

For Russian-born Turlov, the attack fell flat because it inadvertently created a can’t-miss buying opportunity for the brokerage’s own clients who double as shareholders.

“That’s not the way I’d want our capitalization to grow,” Turlov said in an interview in Almaty, the former Kazakh capital he calls home. “The reason is that what led to the increase in the price of our shares wasn’t our strength, but someone else’s mistake.”

Hindenburg declined to comment for this story.

Though the Nasdaq-listed stock has remained volatile, it’s up by almost 45% so far this year and gained about 11% since the last trading session before Hindenburg’s publication on Aug. 15. Shares out on loan, an indication of short interest, peaked in mid-August at just over 6% of the free float and has more than halved since then, according to data from S&P Global Market Intelligence.

The clash that played out in the market has done little to sway Hindenburg, which said it took a short position in Freedom’s shares after a yearlong investigation into the company. Nate Anderson, the researcher’s founder, has continued to argue on social media that the equity is worthless and accused Turlov himself of “buying up the float.”

The publication and its aftermath crystallized some concerns around a company that’s grown at breakneck speed, more than doubling its total assets and brokerage customer accounts in the two years through March 31.

The Kazakh regulator said in a statement in late August that it concluded some of the Freedom group’s transactions involving government securities and bonds of a central bank unit were committed “for the purpose of manipulation.” The company is now being investigated by the US Department of Justice and the Securities and Exchange Commission, according to CNBC.

Freedom has been approached for clarification by “approximately everyone,” including Kazakh and US regulators since Hindenburg’s report, according to Turlov, who described the requests as “fact-finding in nature.” While not commenting on any regulatory proceedings, Turlov said his company expects no material consequences as a result and doesn’t anticipate that any charges will be brought against it.

The scrutiny will increase as Freedom expands its footprint in the US and western Europe, markets that now generate 10% of its total revenue. The stock is up almost 600% since an initial public offering in 2019.

This year, it agreed to buy New-York based financial services firm Maxim Group in a cash-and-stock deal worth about $400 million, alongside other recent acquisitions in the US that included broker Prime Executions Inc. and LD Micro, a conference platform for small-cap issuers. The company has offices across Europe and central Asia as well as in the US.

S&P Global Ratings has said a “rising number” of European Union citizens is adding to a customer base that now primarily consists of Kazakhs, Ukrainians and unsanctioned Russians. Freedom sold its Russian operations following last year’s invasion of Ukraine and Turlov gave up his Russian citizenship.

Days after Hindenburg’s publication, S&P put Freedom’s long-term rating on credit watch negative, faulting its “weak compliance and reporting mechanisms.”

On Oct. 31, the rating company affirmed its rating with a negative outlook, saying the “immediate fallout” from Hindenburg’s allegations “was relatively contained.” But it also warned that “although reputation and regulatory risks appear to have diminished, the possibility of future adverse developments over the longer term cannot be fully ruled out.”

The showdown with Hindenburg, in Turlov’s telling, was decided once Freedom’s clients became net buyers. The selloff was over after two days and then the stock took off on Aug. 18, skyrocketing by over 25%.

What happened, Turlov said, is known as a short squeeze — meaning traders who were betting against his company had to cover their positions at a higher price, leading to a rebound in the stock. By the end of August, the stock hit a record high of just over $100 per share.

Turlov said neither he nor the company bought the shares. He owned the same number of Freedom shares on Sept. 8 as before the short seller’s attack and any purchases would have required regulatory disclosure. Freedom’s insider trading policies around financial reporting also meant management was forbidden from buying the company’s stock, he said.

Turlov is also adamant that Freedom’s clients purchased the stock with their own money, though the information couldn’t be verified. “Clients may have seen this as a chance to even make money at a time of general panic,” he said.

Despite a limited free float, Turlov said Freedom has over 10,000 shareholders. Those that bought the dip — including several large clients — reaped a quick profit that Turlov estimates at “several tens” of millions of dollars.

Prior to Freedom, Hindenburg had targeted some 30 companies since 2020, knocking their stocks down about 15% on average in the day that followed. That’s roughly double the decline in Freedom’s shares in the two days after the short seller’s attack.

Hindenburg’s biggest oversight, according to Turlov, was in “underestimating our shareholder structure and the level of trust our clients have in us.”

‘Trusting Relationship’

“Unlike many public companies, we know a lot of our shareholders personally,” he said.

The activist short seller, whose recent high-profile targets have included the likes of Carl Icahn and Gautam Adani, was the most formidable adversary yet for Turlov, in a career already dogged by accusations and scrutiny.

Freedom has responded to past criticism by saying its business is in line with market practice, a view repeated by Turlov. The company called Hindenburg’s report “speculation and a set of unsubstantiated facts.”

Notwithstanding the stock’s rebound, Turlov says the experience brought something of a reckoning for his company.

Freedom is aiming to hire a chief risk officer as well as a chief legal officer by the end of 2023. It’s part of an effort that also includes a plan to issue a forensic report by year-end that will examine the accusations made by Hindenburg.

--With assistance from Tom Maloney.