Emerging Asian central banks are turning to innovative ways to protect their currencies as fears over higher-for-longer US interest rates and rising global tensions drag down risk assets.

Asian currencies are especially exposed to outflows as benchmark rates in the region are generally lower than their emerging peers, resulting in a wider differential with the US.

Among some of the ways officials are countering that: Indian policymakers said this month they’re looking to sell more bonds to soak up cash, which should bolster the rupee. Their Indonesian peers in September started issuing a new line of debt to attract inflows and underpin the currency. China is selling a record amount of local-currency sovereign debt offshore to raise yuan demand.

Indonesia and India are issuing more of their higher-yielding bonds to encourage inflows, which “is a new way where they can still support the currencies without having to use foreign-exchange reserves,” said Eddie Cheung, a senior emerging markets strategist at Credit Agricole CIB in Hong Kong. “I think that’s playing it quite smart.”

The use of creative ways to support their currencies is one way out of the dilemma of having to choose between allowing a currency to weaken, burning through reserves, or raising rates and crimping economic growth.

Bloomberg’s dollar index has surged more than 6% from its July low as traders have boosted bets on higher Fed rates amid sticky inflation and robust US economic data. At the same time, the war in Ukraine and the Israel-Hamas conflict are pushing up oil prices, driving haven demand for the greenback.

The outlook for Asia currencies is a big deal for global emerging-market indexes. The yuan, rupee and rupiah have a collective weighting of 45% in the MSCI EM Currency Index. China and India’s government bonds make up a combined 22.2% of the JPMorgan Government Bond Index-Emerging Markets, according to a representative from the US bank.

Depleting Stockpiles

India’s falling foreign-currency reserves suggest the central bank has been dipping into its stockpiles this year to bolster its currency. Policymakers took another step at their Oct. 6 meeting by announcing a potential bond-sale plan to mop up extra cash and support the rupee by pushing up yields.

The measures employed by India so far have largely succeeded as the rupee has been virtually unchanged this year even as most of its emerging peers have weakened.

Indonesia’s central bank began selling so-called Bank Indonesia Rupiah Securities in mid-September with the goal of luring in more inflows. The bills, known as SRBI, allow global investors to take short-term currency risk exposure. They were introduced as the nation saw outflows of $1.1 billion from Indonesian bonds last month, the most in almost a year.

‘Creative Complements’

The measures from India and Indonesia “make for very creative complements to currency support that also take into consideration judicious use of FX reserves,” said Vishnu Varathan, head of economics and strategy at Mizuho Bank Ltd. in Singapore. “Especially given that reserve drawdown can be a double-edged sword that suddenly accentuates a selloff if it presents worries about a possible cash-burn.”

China is employing a range of measures to buttress its currency. The government this week announced a 26 billion yuan ($3.6 billion) issue of yuan-denominated sovereign bonds for this quarter, boosting its 2023 total to a record 55 billion yuan. Investors see the main goal of the issuance is to support the yuan by raising demand for the currency.

The People’s Bank of China last month intervened in the offshore yuan market, increasing the cost for banks to borrow the currency from each other in Hong Kong to make it less attractive to bet against it.

Hedging Issues

Some of these measures come with their own costs. In China’s case, investors who own the nation’s bonds are finding it more difficult to hedge as cash rates increase.

“China bonds were suddenly no longer attractive to us when the PBOC abruptly jacked up their offshore cash rates,” said Robert Samson, co-head of global multi-asset at Nikko Asset Management in Singapore. “If you can’t hedge it and you’ve got concerns about the currency, I don’t know how you own it.”

While the various creative measures don’t totally replace the use of foreign-exchange reserves, they do help reduce the amount needed.

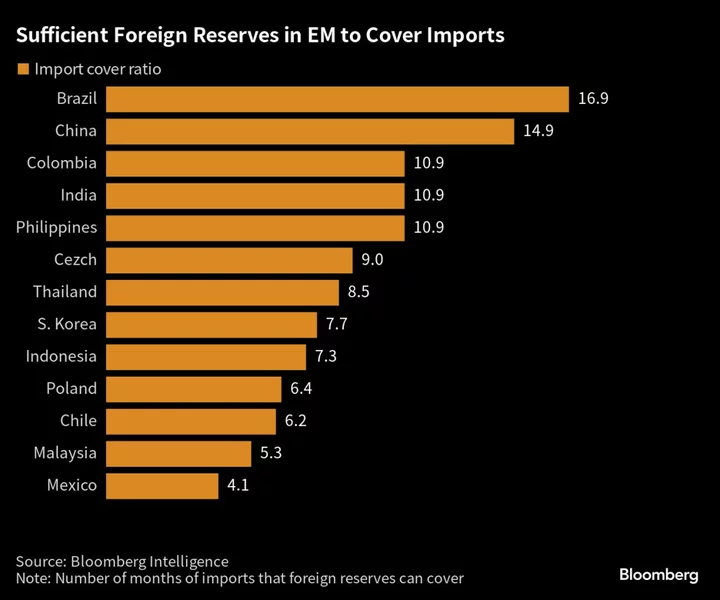

Most emerging-market central banks have an import cover ratio — the number of months of imports that foreign reserves can cover — well above the traditional rule of thumb of three months.

“Reserve adequacy isn’t a concern across most of Asia,” said Arindam Sandilya, head of emerging Asia local markets strategy at JPMorgan Chase Bank in Singapore. “There are variations across countries, but for the most part, they are well in excess of prudential norms.”

What to Watch

- China will release third-quarter GDP Wednesday, with economists expecting growth to decelerate to 4.5% year-on-year. Nation will also industrial production, retail sales and fixed asset investment figures the same day

- Bank Indonesia and Bank of Korea are both forecast to keep rates unchanged Thursday

- Malaysia, Thailand and Mexico all release foreign-reserves data next week, while Malaysia and Poland will publish inflation figures

--With assistance from Subhadip Sircar, Karl Lester M. Yap and Colleen Goko.